Developer Gamma-gamma model PyMC implementation#

Reference:Fader, P. S., & Hardie, B. G. (2013). The Gamma-Gamma model of monetary value. February, 2, 1-9.

http://www.brucehardie.com/notes/025/gamma_gamma.pdf

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pymc as pm

import pytensor.tensor as pt

import seaborn as sns

from pymc_marketing import clv

Simulate data#

rng = np.random.default_rng(42)

# Hyperparameters

p_true = 6.

q_true = 4.

v_true = 15.

# Number of subjects

N = 500

# Subject level parameters

nu_true = pm.draw(pm.Gamma.dist(q_true, v_true, size=N), random_seed=rng)

# Number of observations per subject

x = rng.poisson(lam=2, size=N) + 1

idx = np.repeat(np.arange(0, N), x)

# Observations

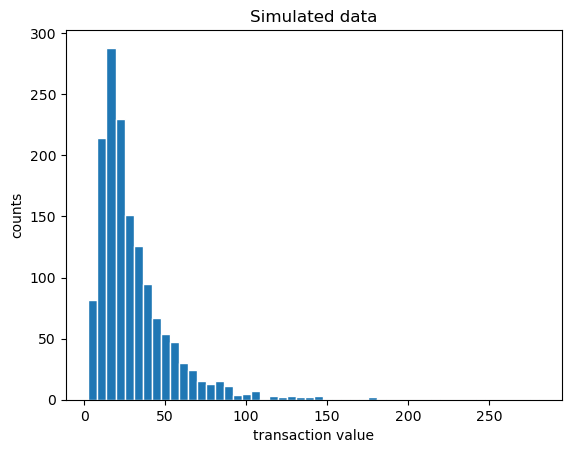

z = pm.draw(pm.Gamma.dist(p_true, nu_true[idx]), random_seed=rng)

print(sum(x))

assert len(nu_true[idx]) == sum(x)

1503

plt.hist(z, bins=50, ec="w")

plt.xlabel("transaction value")

plt.ylabel("counts")

plt.title("Simulated data");

df = pd.DataFrame(data={"individual_transaction_value": z, "customer_id": idx})

z_mean = df.groupby("customer_id").mean()["individual_transaction_value"].values

z_mean[:10]

array([ 17.5597973 , 41.05272046, 15.90609488, 83.95307047,

20.36896009, 23.8572992 , 46.09000842, 47.49876237,

131.16095313, 16.42659393])

PyMC implementation#

We can use the pre-built PyMMMC implementation of the Gamma-Gamma model, which also provides nice ploting and prediction methods

Using individual transactions 𝑧#

model = clv.GammaGammaModelIndividual(data = df)

model

Gamma-Gamma Model (Individual Transactions)

p ~ HalfFlat()

q ~ HalfFlat()

v ~ HalfFlat()

nu ~ Gamma(q, f(v))

spend ~ Gamma(p, f(nu))

model.build_model()

model.graphviz()

model.fit(random_seed=rng)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [p, q, v, nu]

100.00% [8000/8000 00:15<00:00 Sampling 4 chains, 0 divergences]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 16 seconds.

arviz.InferenceData

-

<xarray.Dataset> Dimensions: (chain: 4, draw: 1000, customer_id: 500) Coordinates: * chain (chain) int64 0 1 2 3 * draw (draw) int64 0 1 2 3 4 5 6 7 ... 993 994 995 996 997 998 999 * customer_id (customer_id) int64 0 1 2 3 4 5 6 ... 494 495 496 497 498 499 Data variables: p (chain, draw) float64 6.043 6.218 6.028 ... 5.783 5.617 5.341 q (chain, draw) float64 3.977 4.26 3.962 ... 4.277 4.209 3.401 v (chain, draw) float64 14.94 15.73 15.36 ... 18.15 18.12 14.57 nu (chain, draw, customer_id) float64 0.204 0.1759 ... 0.1358 Attributes: created_at: 2022-12-15T08:50:41.657496 arviz_version: 0.14.0 inference_library: pymc inference_library_version: 5.0.0 sampling_time: 15.84934139251709 tuning_steps: 1000 -

<xarray.Dataset> Dimensions: (chain: 4, draw: 1000) Coordinates: * chain (chain) int64 0 1 2 3 * draw (draw) int64 0 1 2 3 4 5 ... 994 995 996 997 998 999 Data variables: (12/17) n_steps (chain, draw) float64 15.0 15.0 15.0 ... 15.0 15.0 max_energy_error (chain, draw) float64 0.6677 -0.3882 ... -1.41 1.565 lp (chain, draw) float64 -5.977e+03 ... -6.014e+03 process_time_diff (chain, draw) float64 0.005394 0.004418 ... 0.006559 tree_depth (chain, draw) int64 4 4 4 4 4 4 4 4 ... 4 4 4 4 4 4 4 index_in_trajectory (chain, draw) int64 8 -9 -6 3 -6 ... 9 -3 -7 11 -13 ... ... energy (chain, draw) float64 6.208e+03 ... 6.283e+03 perf_counter_start (chain, draw) float64 2.382e+03 ... 2.387e+03 reached_max_treedepth (chain, draw) bool False False False ... False False acceptance_rate (chain, draw) float64 0.6662 0.9528 ... 0.9918 0.559 step_size_bar (chain, draw) float64 0.2451 0.2451 ... 0.2524 0.2524 step_size (chain, draw) float64 0.2618 0.2618 ... 0.2271 0.2271 Attributes: created_at: 2022-12-15T08:50:41.673955 arviz_version: 0.14.0 inference_library: pymc inference_library_version: 5.0.0 sampling_time: 15.84934139251709 tuning_steps: 1000 -

<xarray.Dataset> Dimensions: (obs: 1503) Coordinates: * obs (obs) int64 0 1 2 3 4 5 6 7 ... 1496 1497 1498 1499 1500 1501 1502 Data variables: spend (obs) float64 14.17 11.38 20.49 24.21 ... 33.88 31.51 49.41 30.51 Attributes: created_at: 2022-12-15T08:50:41.680915 arviz_version: 0.14.0 inference_library: pymc inference_library_version: 5.0.0

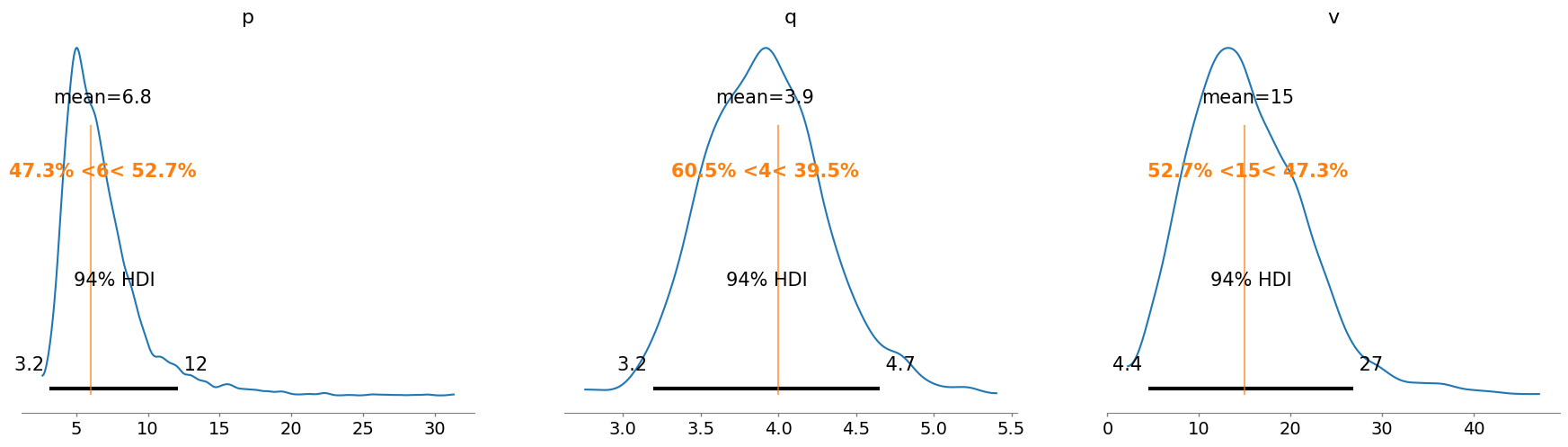

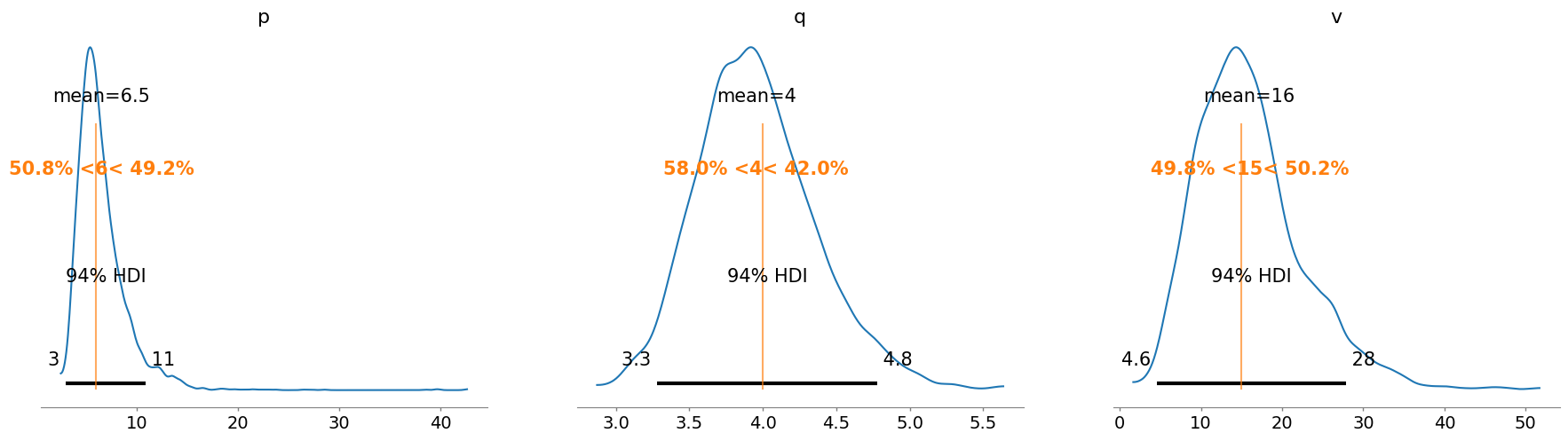

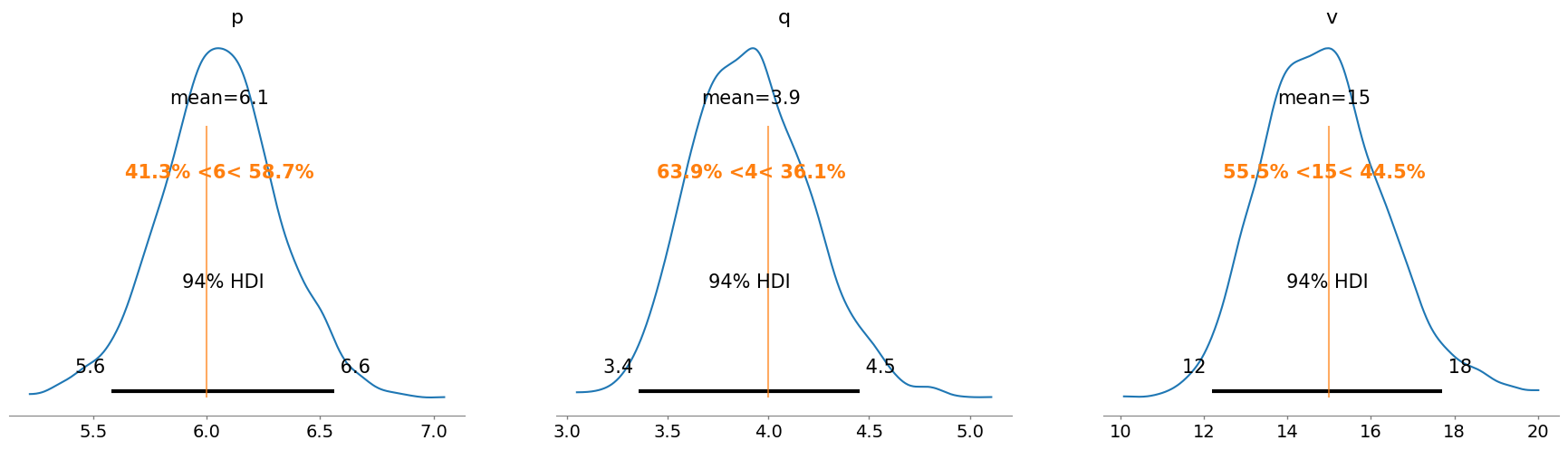

az.plot_posterior(model.fit_result, var_names=["p", "q", "v"], ref_val=[p_true, q_true, v_true]);

expected_spend = model.expected_customer_spend(

customer_id=idx,

individual_transaction_value=z,

).stack(sample=("draw", "chain"))

Sampling: [nu]

100.00% [4000/4000 00:00<00:00]

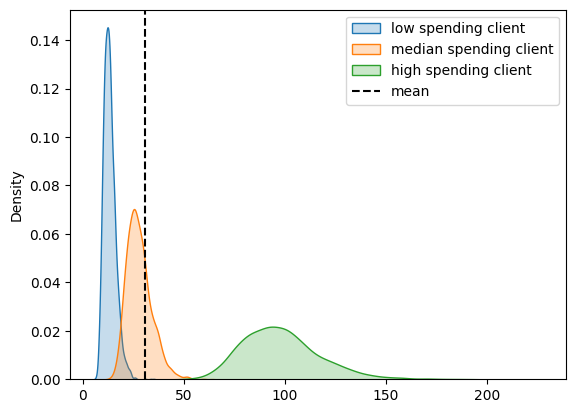

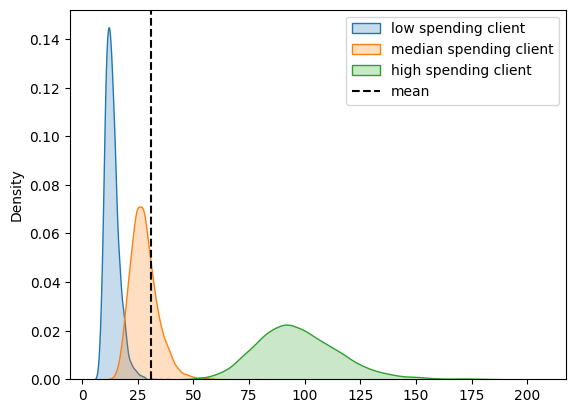

# Choose 10 lowest, median and 10 highest spending clients

selected_idxs = np.argsort(nu_true)[::-1][[10, 250, -10]]

selected_idxs

array([267, 407, 359])

sns.kdeplot(expected_spend.sel(customer_id=selected_idxs[0]), fill=True, label="low spending client")

sns.kdeplot(expected_spend.sel(customer_id=selected_idxs[1]), fill=True, label="median spending client")

sns.kdeplot(expected_spend.sel(customer_id=selected_idxs[2]), fill=True, label="high spending client")

plt.axvline(expected_spend.mean(), color="k", ls="--", label="mean")

plt.legend();

new_spend = model.expected_new_customer_spend().stack(sample=("chain", "draw"))

Sampling: [nu]

100.00% [4000/4000 00:00<00:00]

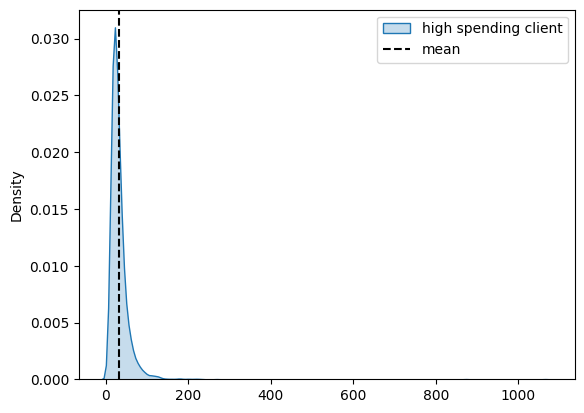

sns.kdeplot(new_spend.isel(new_customer_id=0), fill=True, label="high spending client")

plt.axvline(new_spend.mean(), color="k", ls="--", label="mean")

plt.legend();

Using average transactions per user \(\overline{z}\)#

model = clv.GammaGammaModel(

customer_id=idx,

mean_transaction_value=z_mean,

frequency=x,

)

model

Gamma-Gamma Model (Mean Transactions)

p ~ HalfFlat()

q ~ HalfFlat()

v ~ HalfFlat()

likelihood ~ Potential(f(q, p, v))

model.fit(random_seed=rng)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [p, q, v]

100.00% [8000/8000 00:19<00:00 Sampling 4 chains, 0 divergences]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 20 seconds.

arviz.InferenceData

-

<xarray.Dataset> Dimensions: (chain: 4, draw: 1000) Coordinates: * chain (chain) int64 0 1 2 3 * draw (draw) int64 0 1 2 3 4 5 6 7 8 ... 992 993 994 995 996 997 998 999 Data variables: p (chain, draw) float64 8.287 6.904 11.12 11.37 ... 5.595 7.243 5.328 q (chain, draw) float64 3.116 3.177 3.585 3.381 ... 3.931 3.953 3.654 v (chain, draw) float64 8.172 10.5 7.579 6.657 ... 16.45 12.56 15.75 Attributes: created_at: 2022-12-15T08:51:18.981662 arviz_version: 0.14.0 inference_library: pymc inference_library_version: 5.0.0 sampling_time: 19.611279487609863 tuning_steps: 1000 -

<xarray.Dataset> Dimensions: (chain: 4, draw: 1000) Coordinates: * chain (chain) int64 0 1 2 3 * draw (draw) int64 0 1 2 3 4 5 ... 994 995 996 997 998 999 Data variables: (12/17) n_steps (chain, draw) float64 63.0 63.0 31.0 ... 63.0 31.0 max_energy_error (chain, draw) float64 6.796 0.5487 ... 0.8002 lp (chain, draw) float64 -2.067e+03 ... -2.063e+03 process_time_diff (chain, draw) float64 0.01295 0.01572 ... 0.006056 tree_depth (chain, draw) int64 6 6 5 5 6 6 4 5 ... 6 4 1 5 5 6 5 index_in_trajectory (chain, draw) int64 16 6 -13 6 -25 ... -1 3 10 -19 -8 ... ... energy (chain, draw) float64 2.071e+03 ... 2.067e+03 perf_counter_start (chain, draw) float64 2.414e+03 ... 2.425e+03 reached_max_treedepth (chain, draw) bool False False False ... False False acceptance_rate (chain, draw) float64 0.241 0.9067 ... 0.991 0.737 step_size_bar (chain, draw) float64 0.06783 0.06783 ... 0.07536 step_size (chain, draw) float64 0.08445 0.08445 ... 0.06033 Attributes: created_at: 2022-12-15T08:51:18.999668 arviz_version: 0.14.0 inference_library: pymc inference_library_version: 5.0.0 sampling_time: 19.611279487609863 tuning_steps: 1000

az.plot_posterior(model.fit_result, var_names=["p", "q", "v"], ref_val=[p_true, q_true, v_true]);

expected_spend = model.expected_customer_spend(

customer_id=idx,

mean_transaction_value=z_mean,

frequency=x,

).stack(sample=("draw", "chain"))

Sampling: [nu]

100.00% [4000/4000 00:01<00:00]

sns.kdeplot(expected_spend.sel(customer_id=selected_idxs[0]), fill=True, label="low spending client")

sns.kdeplot(expected_spend.sel(customer_id=selected_idxs[1]), fill=True, label="median spending client")

sns.kdeplot(expected_spend.sel(customer_id=selected_idxs[2]), fill=True, label="high spending client")

plt.axvline(expected_spend.mean(), color="k", ls="--", label="mean")

plt.legend();

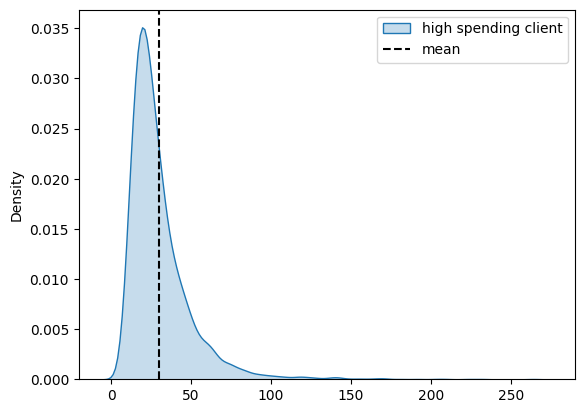

new_spend = model.expected_new_customer_spend().stack(sample=("chain", "draw"))

Sampling: [nu]

100.00% [4000/4000 00:00<00:00]

sns.kdeplot(new_spend.isel(new_customer_id=0), fill=True, label="high spending client")

plt.axvline(new_spend.mean(), color="k", ls="--", label="mean")

plt.legend();

Manual PyMC implementations#

We show how the Gamma-Gamma model can be implemented by hand using PyMC. This clarifies how the model can be modified or extended to include more prior information or additional structure.

Gamma-Gamma model conditioned on individual transactions \(z\)#

with pm.Model() as m1:

p = pm.HalfFlat("p")

q = pm.HalfFlat("q")

v = pm.HalfFlat("v")

nu = pm.Gamma("nu", q, v, size=N)

pm.Gamma("z", p, nu[idx], observed=z)

pm.Deterministic("mean_spend", p / nu)

trace1 = pm.sample(random_seed=rng)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [p, q, v, nu]

100.00% [8000/8000 00:20<00:00 Sampling 4 chains, 0 divergences]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 21 seconds.

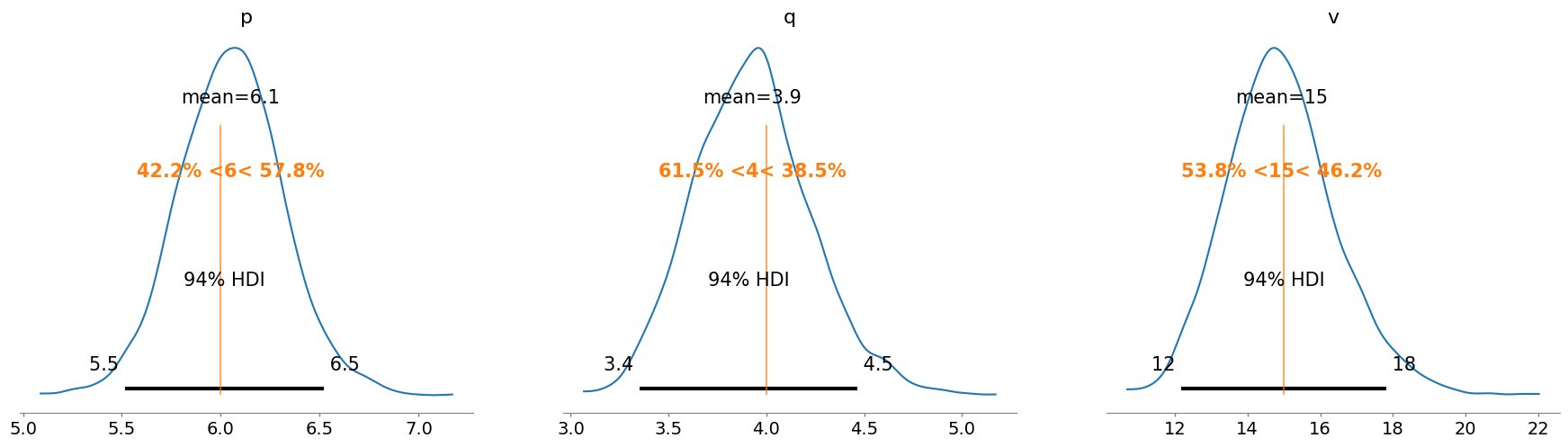

az.summary(trace1, var_names=["p", "q", "v"])

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| p | 6.055 | 0.260 | 5.578 | 6.564 | 0.020 | 0.014 | 178.0 | 382.0 | 1.02 |

| q | 3.914 | 0.295 | 3.358 | 4.453 | 0.007 | 0.005 | 1877.0 | 1959.0 | 1.00 |

| v | 14.879 | 1.486 | 12.194 | 17.717 | 0.071 | 0.050 | 438.0 | 1131.0 | 1.01 |

az.plot_posterior(trace1, var_names=["p", "q", "v"], ref_val=[p_true, q_true, v_true]);

Gamma-gamma model conditioned on average transactions per user \(\overline{z}\)#

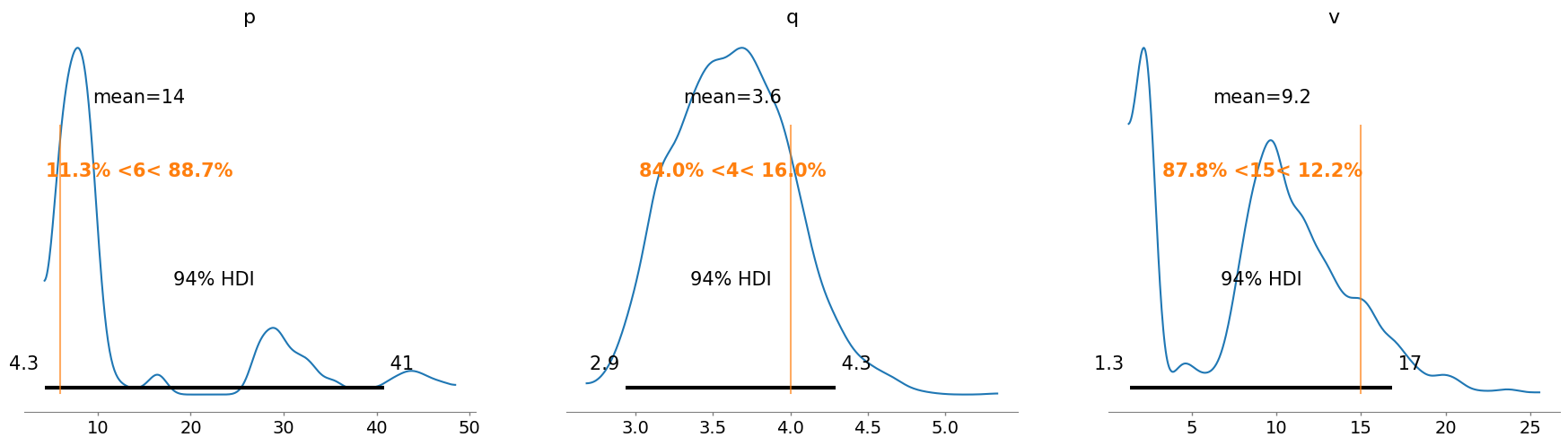

This fails to sample because the model contains “nearly” two independent parameters per observation. For more details check this Discourse topic

with pm.Model() as m2:

p = pm.HalfFlat("p")

q = pm.HalfFlat("q")

v = pm.HalfFlat("v")

nu = pm.Gamma("nu", q, v, size=N)

# We use the convolution properties of the gamma distribution to model

# the mean of multiple transaction using the parameters of individual

# transactions

pm.Gamma("z_mean", p*x, nu*x, observed=z_mean)

trace2 = pm.sample(random_seed=rng)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [p, q, v, nu]

100.00% [8000/8000 00:26<00:00 Sampling 4 chains, 0 divergences]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 27 seconds.

az.summary(trace2, var_names=["p", "q", "v"])

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| p | 14.454 | 11.819 | 4.299 | 40.762 | 5.738 | 4.375 | 5.0 | 11.0 | 2.17 |

| q | 3.629 | 0.376 | 2.939 | 4.294 | 0.129 | 0.094 | 8.0 | 41.0 | 1.41 |

| v | 9.154 | 5.062 | 1.340 | 16.853 | 2.264 | 1.705 | 5.0 | 11.0 | 2.09 |

az.plot_posterior(trace2, var_names=["p", "q", "v"], ref_val=[p_true, q_true, v_true]);

Gamma-Gamma model conditioned on average transaction per user with \(\nu\) marginalized#

with pm.Model() as m3:

p = pm.HalfFlat("p")

q = pm.HalfFlat("q")

v = pm.HalfFlat("v")

# Likelihood of z_mean, marginalizing over nu

likelihood = pm.Potential(

"likelihood",

(

pt.gammaln(p * x + q)

- pt.gammaln(p * x)

- pt.gammaln(q)

+ q * pt.log(v)

+ (p * x - 1) * pt.log(z_mean)

+ (p * x) * pt.log(x)

- (p * x + q) * pt.log(x * z_mean + v)

),

)

# Closed form solution posterior individual nu

nu = pm.Deterministic("nu", pm.Gamma.dist(p * x + q, v + x * z_mean))

pm.Deterministic("mean_spend", p / nu)

trace3 = pm.sample(random_seed=rng)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [p, q, v]

100.00% [8000/8000 00:32<00:00 Sampling 4 chains, 0 divergences]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 33 seconds.

az.summary(trace3, var_names=["p", "q", "v"])

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| p | 6.845 | 2.937 | 3.153 | 12.110 | 0.110 | 0.080 | 865.0 | 812.0 | 1.0 |

| q | 3.915 | 0.390 | 3.194 | 4.654 | 0.012 | 0.009 | 974.0 | 1118.0 | 1.0 |

| v | 15.375 | 6.510 | 4.445 | 26.879 | 0.221 | 0.156 | 816.0 | 738.0 | 1.0 |

az.plot_posterior(trace3, var_names=["p", "q", "v"], ref_val=[p_true, q_true, v_true]);