MMM with time-varying media baseline#

Introduction#

In the domain of Marketing Mix Modeling (MMM), understanding the impact of various marketing activities on a target variable and other key performance indicators is crucial. Traditional regression models often neglect the temporal dynamics of marketing activities, potentially leading to biased or incomplete insights. This notebook aims to showcase the difference between a conventional regression model that does not account for time variation and a more sophisticated model that incorporates time as a key component through a Gaussian process.

The objective is to determine the contribution of each marketing activity to the overall target variable or desired outcome. This process typically involves two critical transformations:

Saturation Function: This function models the diminishing returns of marketing inputs. As more resources are allocated to a specific channel, the incremental benefit tends to decrease.

Adstock Function: This function captures the carryover effect of marketing activities over time, recognizing that the impact of a marketing effort extends beyond the immediate period in which it occurs.

The standard approach in MMM applies these transformations to the marketing inputs, resulting in a contribution to the outcome.

Time-Dependent MMM Model#

In real-world scenarios, the effectiveness of marketing activities is not static but varies over time due to factors like competitive actions, and market dynamics. To account for this, we introduce a time-dependent component into the MMM framework using a Gaussian Process, specifically a Hilbert Space GP. This allows us to capture the hidden latent temporal variation of the marketing contributions.

Model Specification#

In pymc-marketing we provide an API for a Bayesian media mix model (MMM) specification following Jin, Yuxue, et al. “Bayesian methods for media mix modeling with carryover and shape effects.” (2017) as a base model. Concretely, given a time series target variable \(y_{t}\) (e.g. sales or conversions), media variables \(x_{m, t}\) (e.g. impressions, clicks or costs) and a set of control covariates \(z_{c, t}\) (e.g. holidays, special events) we consider a linear model of the form

where \(\alpha\) is the intercept, \(f\) is a media transformation function and \(\varepsilon_{t}\) is the error term which we assume is normally distributed. The function \(f\) encodes the contribution of media on the target variable. Typically we consider two types of transformation: adstock (carry-over) and saturation effects.

When time_media_varying is set to True, we capture a single latent process that multiplies all channels. We assume all channels share the same time-dependent fluctuations, contrasting with implementations where each channel has an independent latent process. The modified model can be represented as:

where \(\lambda_{t}\) is the time-varying component modeled as a latent process. This shared time-dependent variation \(\lambda_{t}\) allows us to capture the overall temporal effects that influence all media channels simultaneously.

Objective#

This notebook will:

Illustrate the formulation of a standard MMM model without time variation.

Extend the model to include a time component using HSGP.

Compare the results and insights derived from both models, highlighting the importance of incorporating time variation in capturing the true impact of marketing activities.

By the end of this notebook, you will have a comprehensive understanding of the advantages of using time-dependent MMM models in capturing the dynamic nature of marketing effectiveness, leading to more accurate and actionable insights.

Prerequisite Knowledge#

The notebook assumes the reader has knowledge of the essential functionalities of PyMC-Marketing. If one is unfamiliar, the “MMM Example Notebook” serves as an excellent starting point, offering a comprehensive introduction to media mix models in this context.

Part I: Data Generation Process#

In Part I of this notebook we focus on the data generating process. We want to construct the target variable \(y_{t}\) (sales) by adding each of the components described in the Business Problem section.

Note: Model components are built out of this notebook, we’ll show how they combine together to generate the target.

Prepare Notebook#

import warnings

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import seaborn as sns

from pymc_extras.prior import Prior

from pymc_marketing.mmm import GeometricAdstock, MichaelisMentenSaturation

from pymc_marketing.mmm.multidimensional import MMM

from pymc_marketing.paths import data_dir

warnings.filterwarnings("ignore")

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [12, 7]

plt.rcParams["figure.dpi"] = 100

%load_ext autoreload

%autoreload 2

%config InlineBackend.figure_format = "retina"

1. Date Range#

First we set a time range for our data. We consider a bit more than 2 years of data at weekly granularity.

# Creating variables

seed: int = sum(map(ord, "Time Media Contributions are amazing"))

rng: np.random.Generator = np.random.default_rng(seed=seed)

# date range

min_date = pd.to_datetime("2018-04-01")

max_date = pd.to_datetime("2021-09-01")

df = pd.read_csv(data_dir / "media_tvp_data.csv", index_col=0)

df["date_week"] = pd.to_datetime(df["date_week"])

n = df.shape[0]

print(f"Number of observations: {n}")

Number of observations: 179

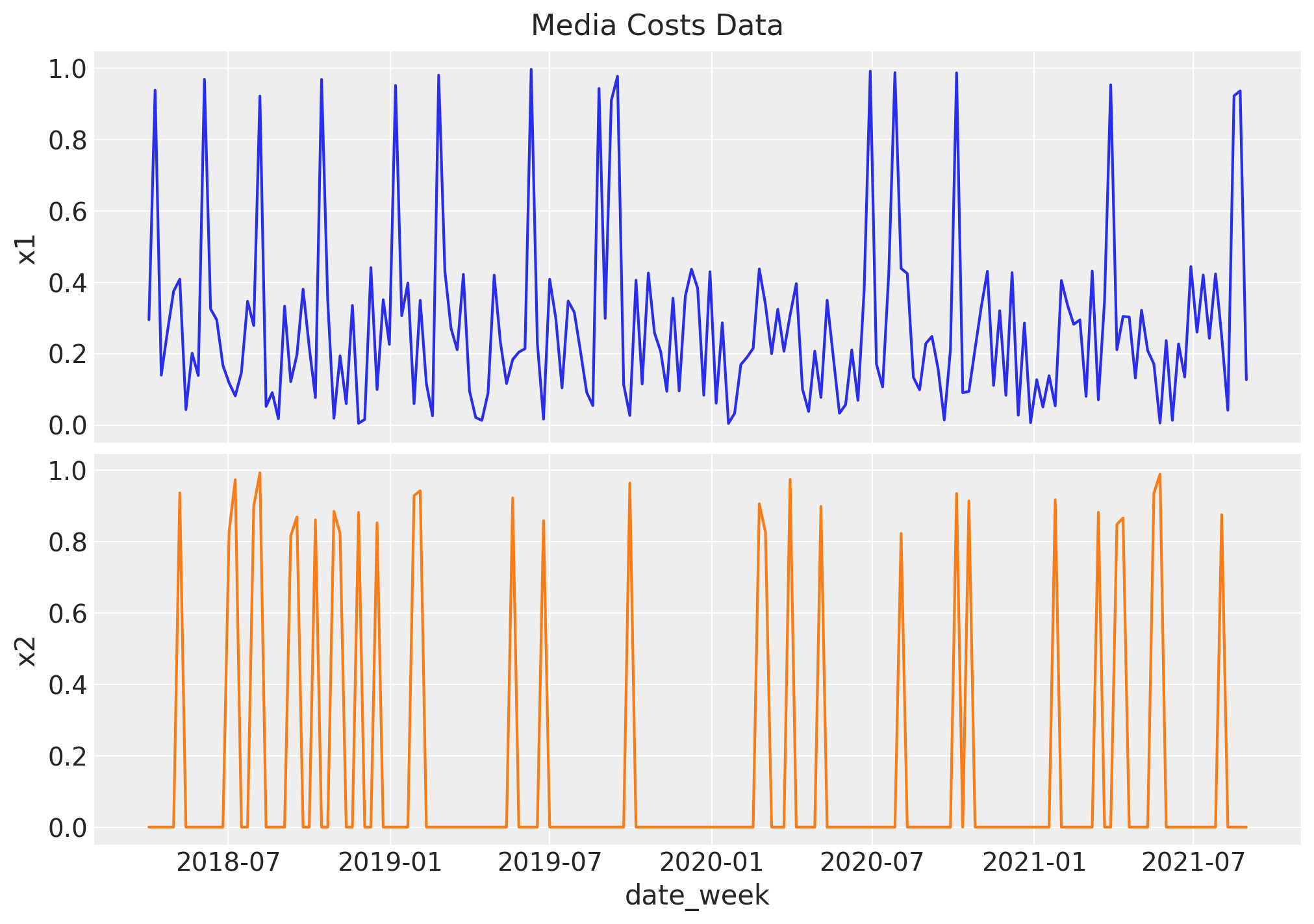

2. Media Costs Data#

Now we generate synthetic data from two channels \(x_1\) and \(x_2\). We refer to it as the raw signal as it is going to be the input at the modeling phase. We expect the contribution of each channel to be different, based on the carryover and saturation parameters.

fig, ax = plt.subplots(

nrows=2, ncols=1, figsize=(10, 7), sharex=True, sharey=True, layout="constrained"

)

sns.lineplot(x="date_week", y="x1", data=df, color="C0", ax=ax[0])

sns.lineplot(x="date_week", y="x2", data=df, color="C1", ax=ax[1])

ax[1].set(xlabel="date_week")

fig.suptitle("Media Costs Data", fontsize=16);

Remark: By design, \(x_{1}\) should resemble a typical paid social channel and \(x_{2}\) a offline (e.g. TV) spend time series.

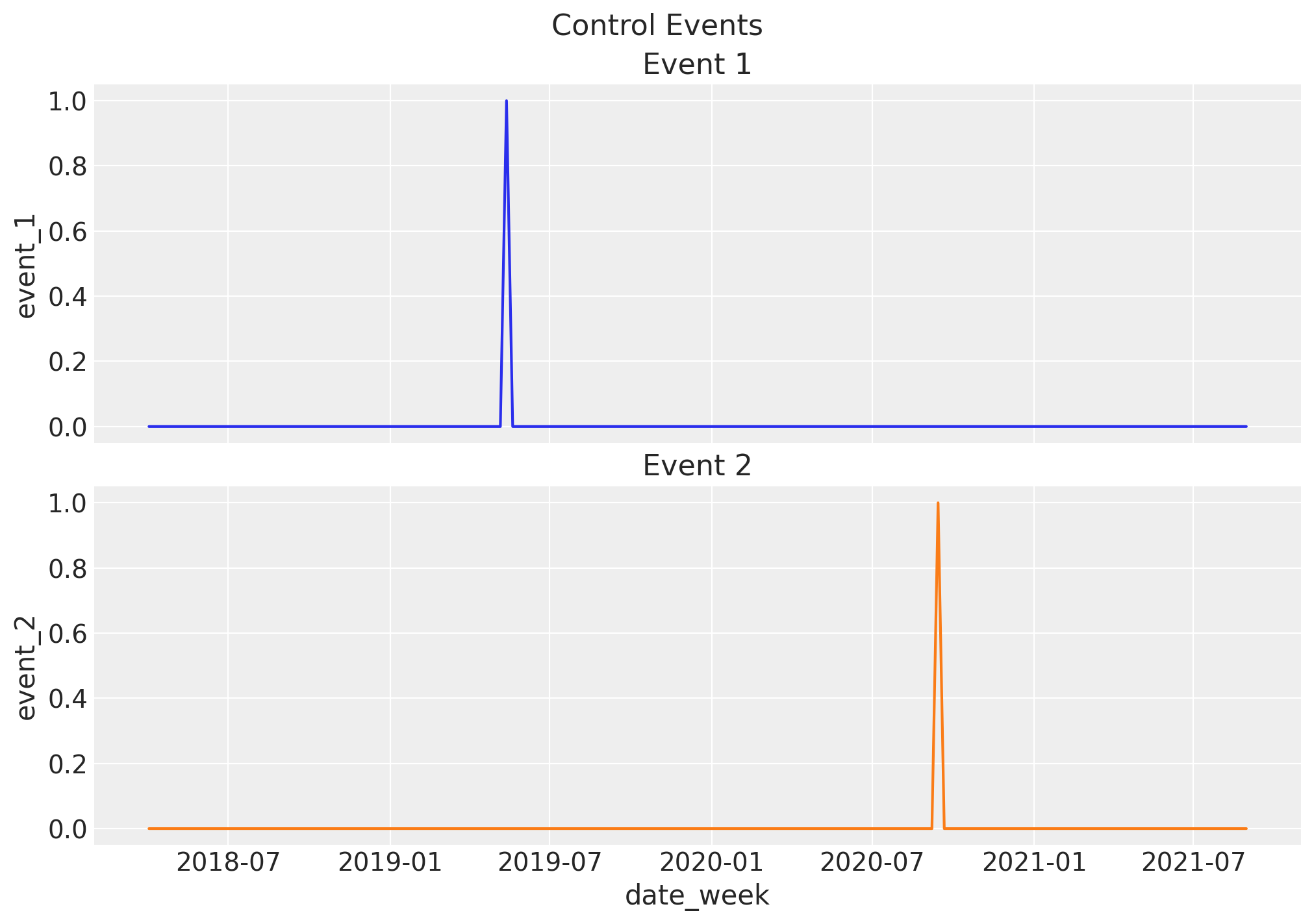

4. Control Variables#

We add two events where there was a remarkable peak in our target variable. We assume they are independent an not seasonal (e.g. launch of a particular product).

fig, ax = plt.subplots(

nrows=2, ncols=1, figsize=(10, 7), sharex=True, sharey=True, layout="constrained"

)

sns.lineplot(x="date_week", y="event_1", data=df, color="C0", ax=ax[0])

ax[0].set_title("Event 1")

sns.lineplot(x="date_week", y="event_2", data=df, color="C1", ax=ax[1])

ax[1].set_title("Event 2")

ax[1].set(xlabel="date_week")

fig.suptitle("Control Events", fontsize=16);

6. Target Variable#

Finally, we need to create our target variable. In order to do create, we’ll use the PyMC do operator to specify some true parameter values that govern the causal relationships in the model.

Doing this, we’ll draw a simulated target variable (sales) \(y\), which assume it is a linear combination of all components in the model. We also add some Gaussian noise.

# Real values

real_alpha = [3, 5]

real_lam = [0.3, 0.5]

adstock_max_lag = 8

yearly_seasonality = 2

true_params = {

"intercept_contribution": 6.0,

"adstock_alpha": np.array([0.5, 0.4]),

"saturation_alpha": np.array(real_alpha),

"saturation_lam": np.array(real_lam),

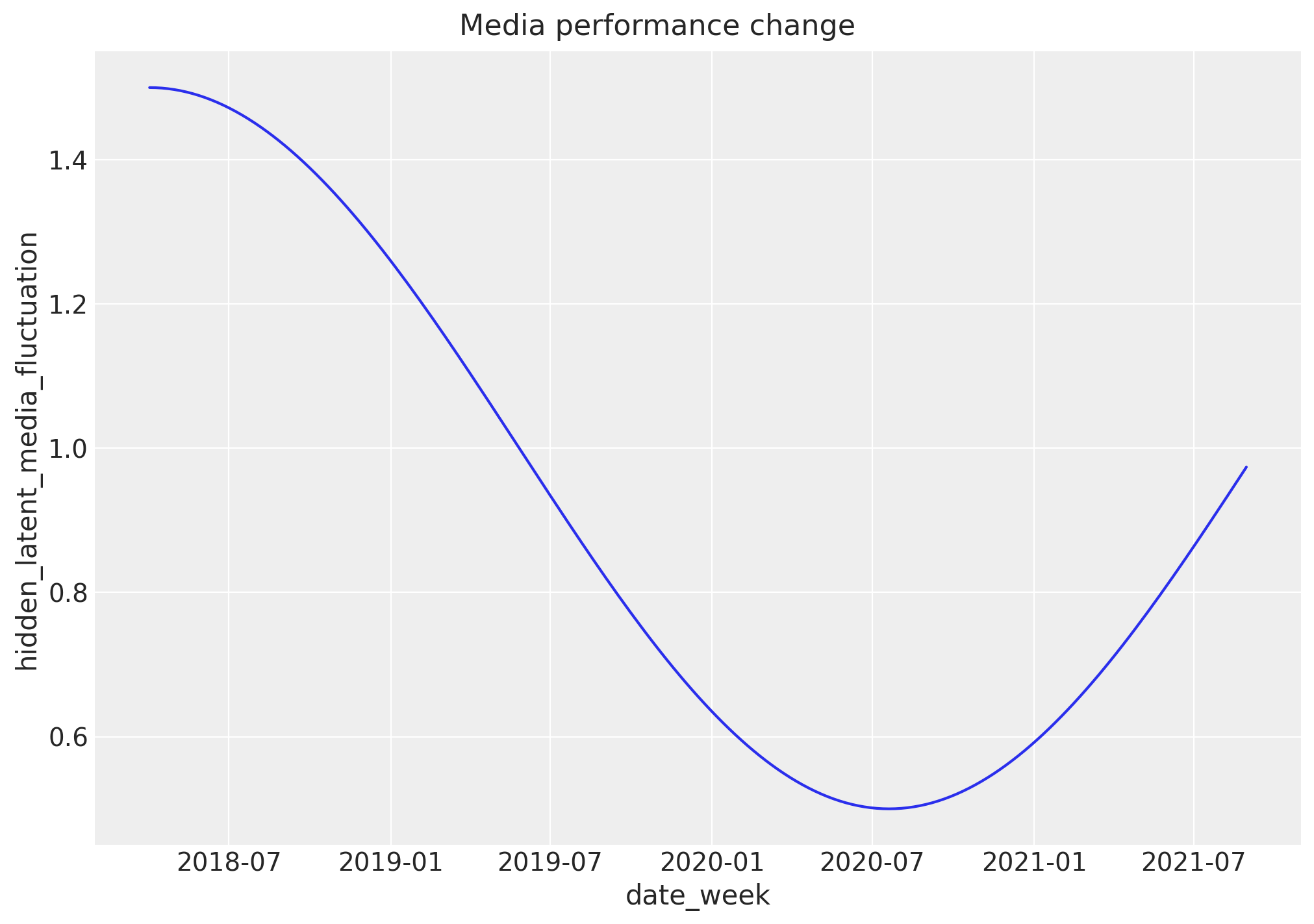

"media_temporal_latent_multiplier": df["hidden_latent_media_fluctuation"],

"gamma_fourier": np.array([2.5, -0.5, 1.5, 2.5]),

"y_sigma": 0.25,

"gamma_control": np.array([-3.5, 6.25]),

}

Using the grid, the do operator, with a dummy model from the MMM class, we can build the true model. We’ll no go into those details, but we can unpack this a little bit.

The do-function takes a pymc.Model object and a dict of parameter values. It then returns a new model where the original random variables (RVs) have been converted to constant nodes taking on the specified values.

Meaning if we pick the node for the intercept, the value should match our grid.

plt.plot(df["intercept"])

plt.title("Intercept Over Time")

plt.xlabel("date_week")

plt.ylabel("Sales (thousands)");

As you can see, the intercept is aligned with the previously added data, having a constant value of 6. But how looks our total contribution after transformed?

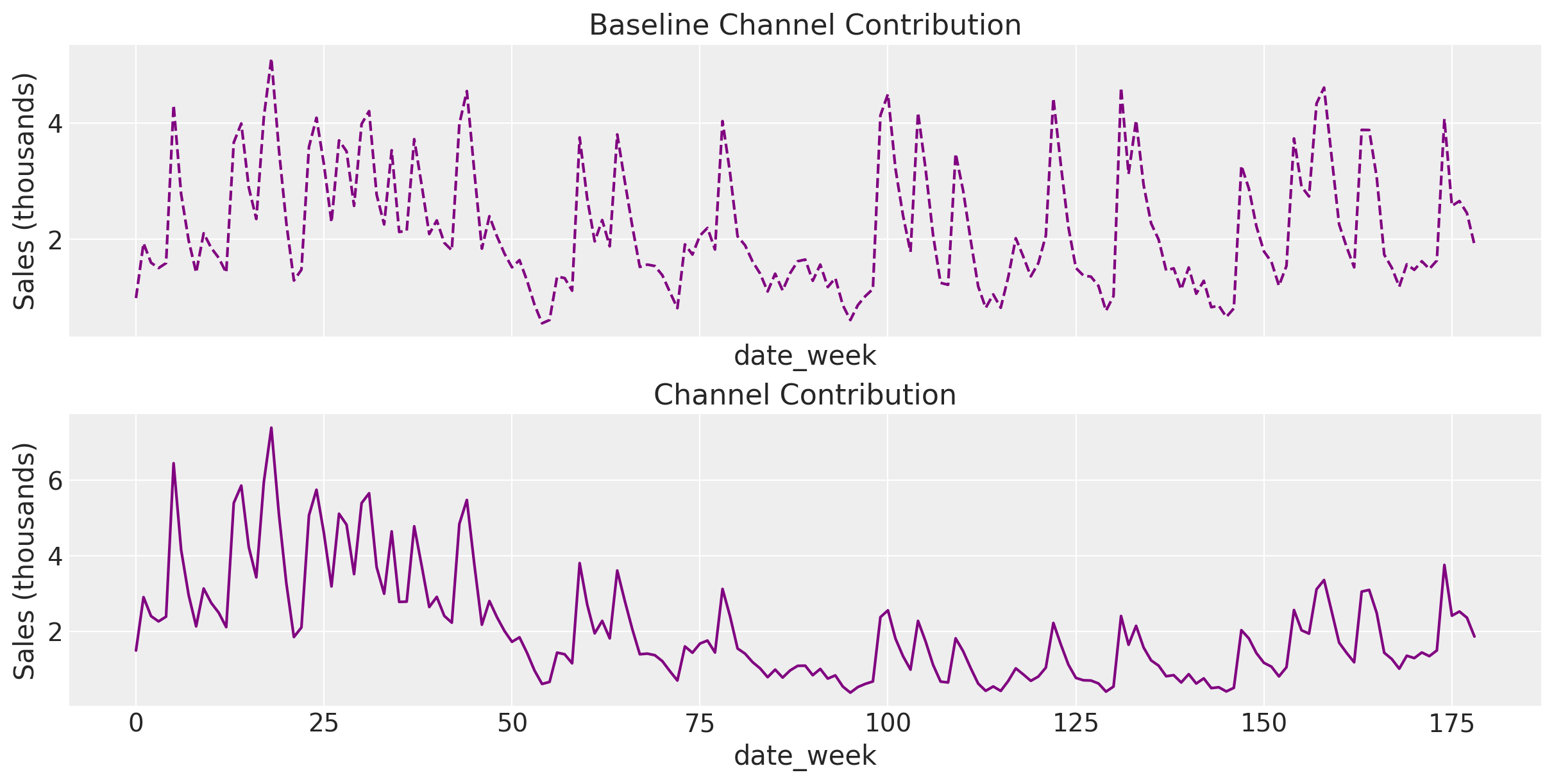

fig, ax = plt.subplots(2, 1, figsize=(12, 6), sharex=True)

ax[0].plot(df["baseline_channel_contribution"], color="purple", linestyle="--")

ax[0].set_title("Baseline Channel Contribution")

ax[0].set_xlabel("date_week")

ax[0].set_ylabel("Sales (thousands)")

ax[1].plot(df["channel_contribution"], color="purple")

ax[1].set_title("Channel Contribution")

ax[1].set_xlabel("date_week")

ax[1].set_ylabel("Sales (thousands)");

Baseline Channel Contributions

The left plot, titled “Baseline Channel Contributions,” shows the contributions of the media channels before considering the time-varying effects. The values are generated by summing the baseline channel contributions drawn from the true model.

Channel Contributions with Time Variation

The right plot, titled “Channel Contributions,” displays the media channel contributions after incorporating the time-varying media performance signal. These contributions reflect the impact of the latent temporal process, represented by hidden_latent_media_fluctuation, which modifies the baseline contributions. This modification captures the natural fluctuations in media performance over time, as influenced by various marketing dynamics.

fig, ax = plt.subplots(

nrows=2, ncols=1, figsize=(10, 7), sharex=True, sharey=True, layout="constrained"

)

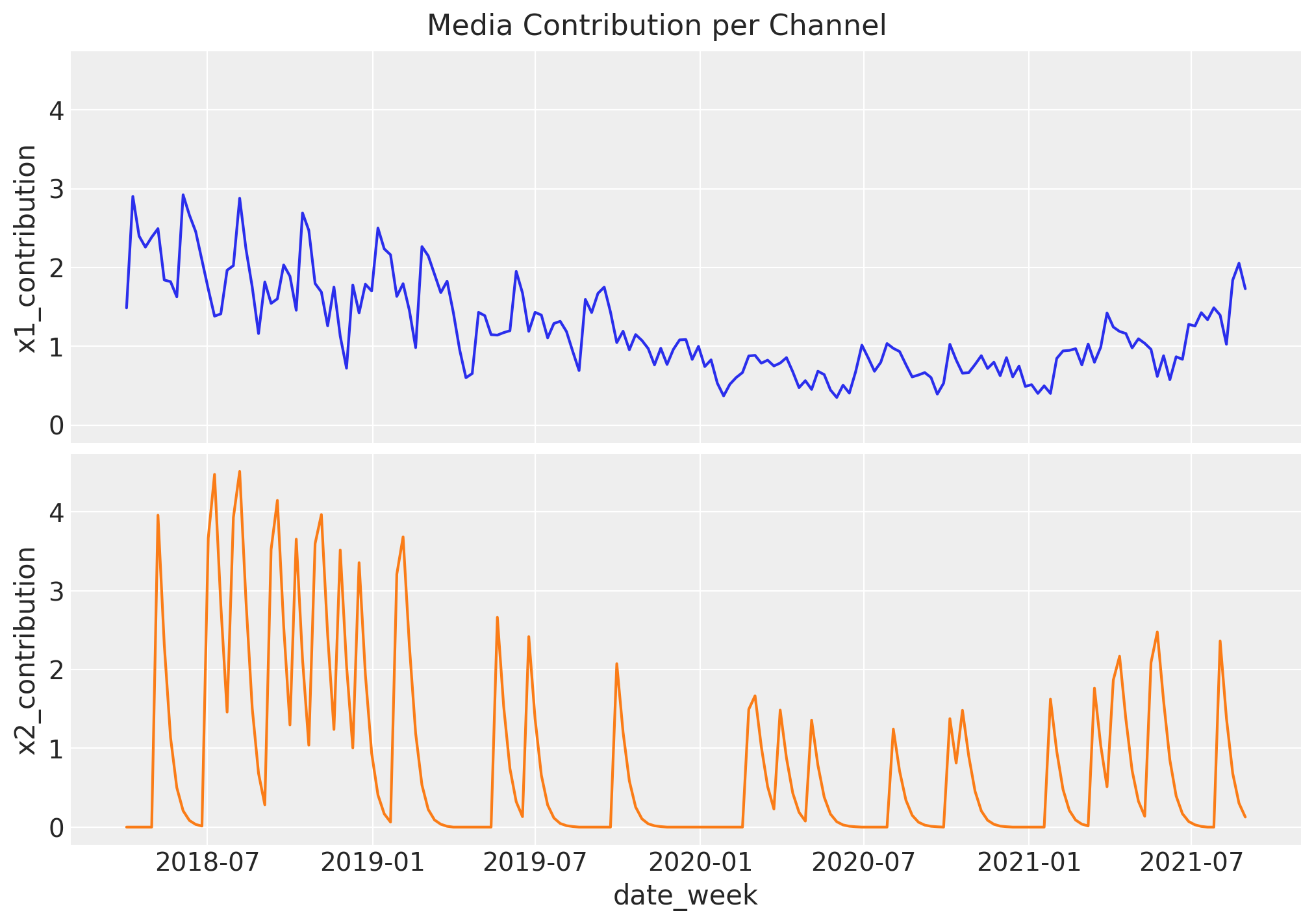

sns.lineplot(x="date_week", y="x1_contribution", data=df, color="C0", ax=ax[0])

sns.lineplot(x="date_week", y="x2_contribution", data=df, color="C1", ax=ax[1])

ax[1].set(xlabel="date_week")

fig.suptitle("Media Contribution per Channel", fontsize=16);

7. Trend & Seasonal Components#

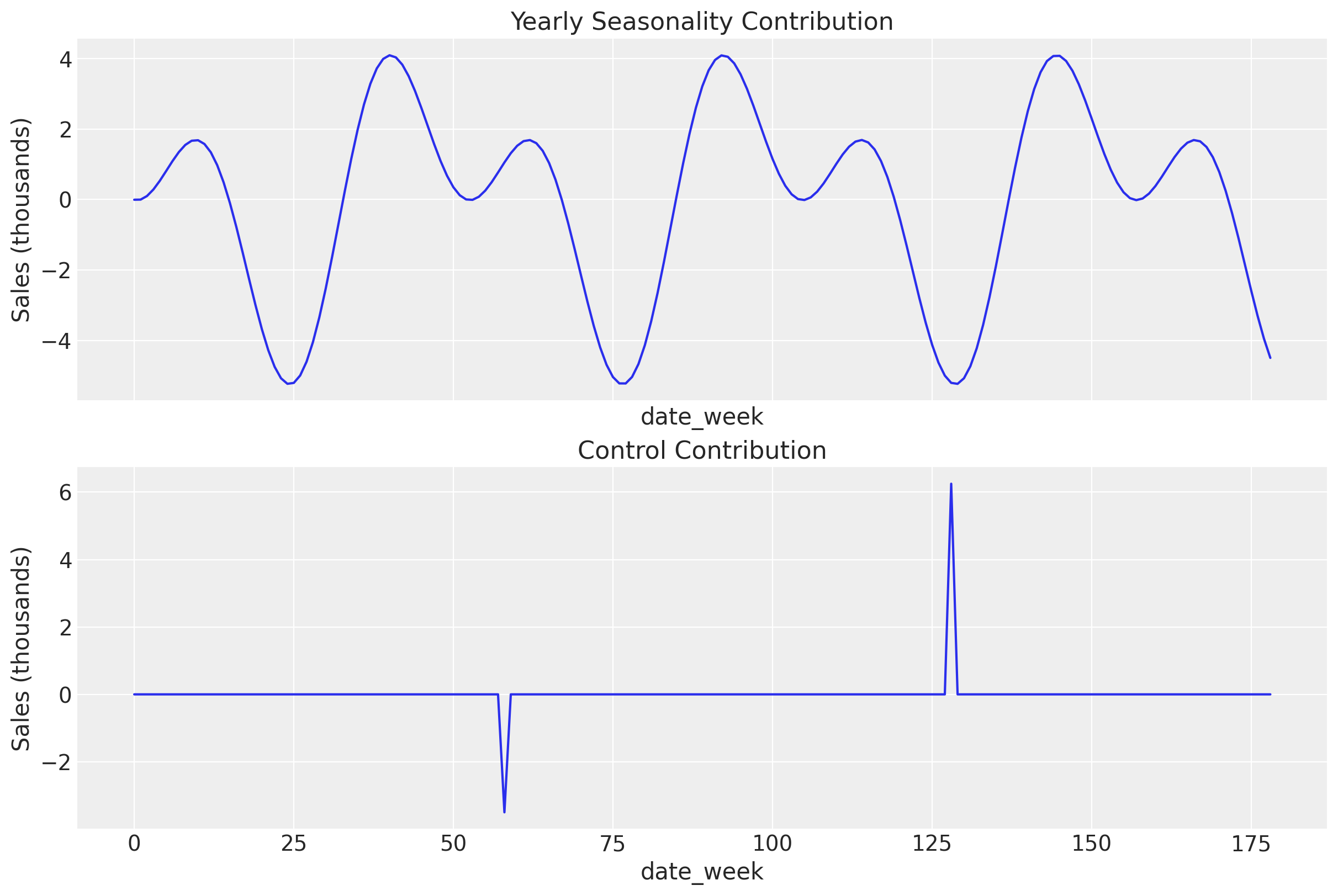

We can also observe the contribution of our control events, as well as the seasonality added when making the true model.

fig, (ax1, ax2) = plt.subplots(nrows=2, ncols=1, figsize=(12, 8), sharex=True)

ax1.plot(df["yearly_seasonality_contribution"])

ax1.set_title("Yearly Seasonality Contribution")

ax1.set_xlabel("date_week")

ax1.set_ylabel("Sales (thousands)")

ax2.plot(df["control_contribution"])

ax2.set_title("Control Contribution")

ax2.set_xlabel("date_week")

ax2.set_ylabel("Sales (thousands)");

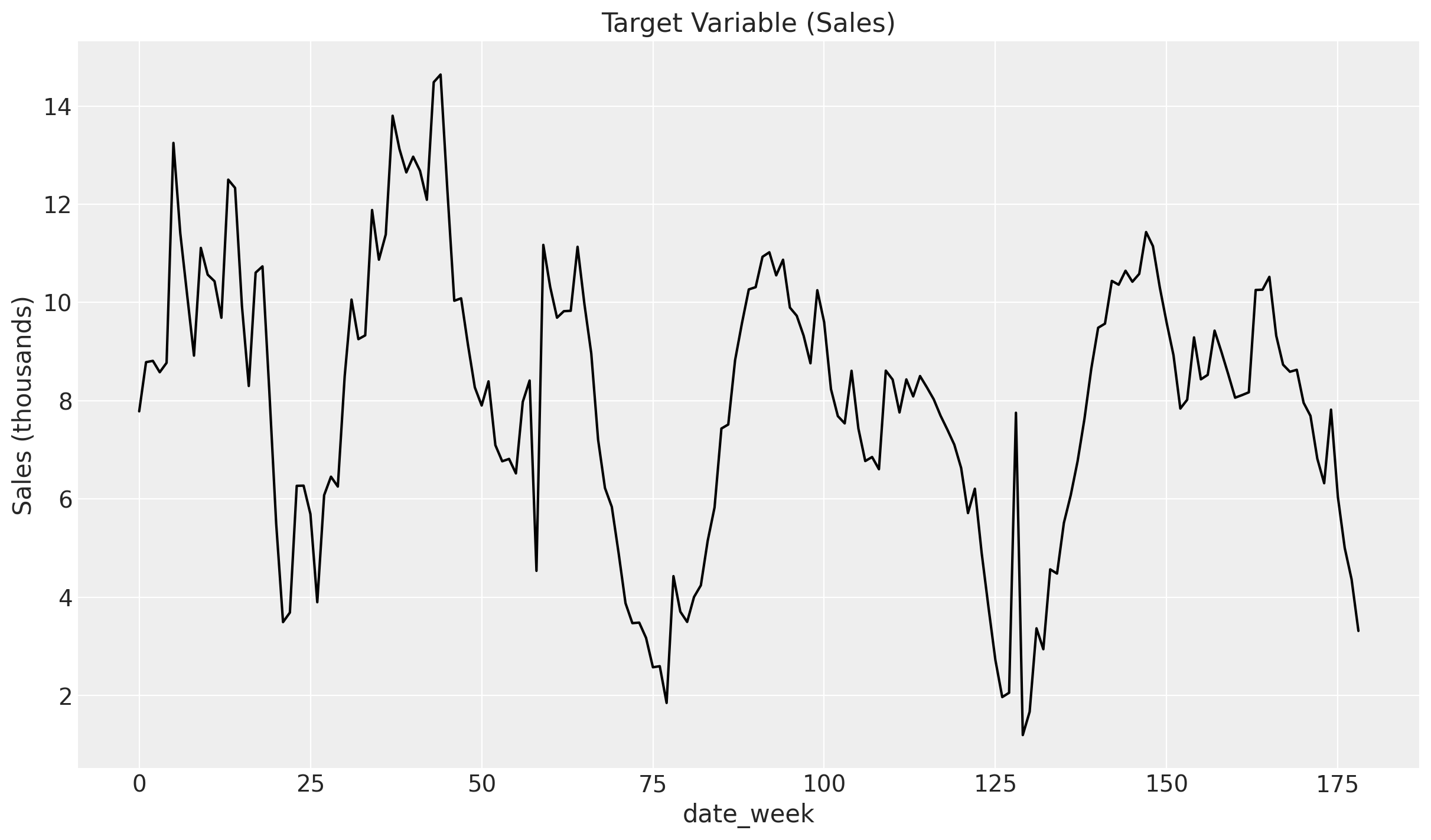

Finally, we can visualize the true target given all the previous componets!

plt.plot(df["y"], color="black")

plt.title("Target Variable (Sales)")

plt.xlabel("date_week")

plt.ylabel("Sales (thousands)");

Now with everything in place, we are going to separate our dataset to leave the real data estimated by the true model inside df and we will create a new dataset called data which will have all the necessary columns but will not have any information about true relationships. Similar to how it would happen in real life.

data = df[["date_week", "x1", "x2", "event_1", "event_2", "y"]].copy()

X = data.drop("y", axis=1)

y = data["y"]

As we discussed previously, we want to compare a model without variant coefficients to see how much it deviates from reality. For this we will create the MMM object that will receive all the necessary parameters to build our model, which should estimate the relationships of the true model.

basic_mmm = MMM(

date_column="date_week",

target_column="y",

channel_columns=["x1", "x2"],

control_columns=["event_1", "event_2"],

yearly_seasonality=yearly_seasonality,

adstock=GeometricAdstock(l_max=adstock_max_lag).set_dims_for_all_priors("channel"),

saturation=MichaelisMentenSaturation().set_dims_for_all_priors("channel"),

)

basic_mmm.fit(

X=X,

y=y,

target_accept=0.92,

draws=500,

random_seed=rng,

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [intercept_contribution, adstock_alpha, saturation_alpha, saturation_lam, gamma_control, gamma_fourier, y_sigma]

Sampling 4 chains for 1_000 tune and 500 draw iterations (4_000 + 2_000 draws total) took 8 seconds.

There were 5 divergences after tuning. Increase `target_accept` or reparameterize.

-

<xarray.Dataset> Size: 26MB Dimensions: (chain: 4, draw: 500, channel: 2, control: 2, fourier_mode: 4, date: 179) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 4kB 0 1 2 ... 498 499 * channel (channel) <U2 16B 'x1' 'x2' * control (control) <U7 56B 'event_1' 'eve... * fourier_mode (fourier_mode) <U5 80B 'sin_1' .... * date (date) datetime64[ns] 1kB 2018-0... Data variables: adstock_alpha (chain, draw, channel) float64 32kB ... gamma_control (chain, draw, control) float64 32kB ... gamma_fourier (chain, draw, fourier_mode) float64 64kB ... intercept_contribution (chain, draw) float64 16kB 0.358... saturation_alpha (chain, draw, channel) float64 32kB ... saturation_lam (chain, draw, channel) float64 32kB ... y_sigma (chain, draw) float64 16kB 0.058... channel_contribution (chain, draw, date, channel) float64 6MB ... control_contribution (chain, draw, date, control) float64 6MB ... fourier_contribution (chain, draw, date, fourier_mode) float64 11MB ... total_media_contribution_original_scale (chain, draw) float64 16kB 489.3... yearly_seasonality_contribution (chain, draw, date) float64 3MB ... Attributes: created_at: 2026-02-03T20:55:06.894079+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 sampling_time: 8.357609987258911 tuning_steps: 1000 pymc_marketing_version: 0.17.1 -

<xarray.Dataset> Size: 264kB Dimensions: (chain: 4, draw: 500) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 4kB 0 1 2 3 4 5 ... 495 496 497 498 499 Data variables: (12/18) acceptance_rate (chain, draw) float64 16kB 0.9822 0.9998 ... 0.9899 divergences (chain, draw) int64 16kB 0 0 0 0 0 0 ... 0 0 0 0 0 0 diverging (chain, draw) bool 2kB False False ... False False energy (chain, draw) float64 16kB -216.4 -220.5 ... -218.7 energy_error (chain, draw) float64 16kB -0.3042 ... 0.04869 index_in_trajectory (chain, draw) int64 16kB 46 -20 -50 -9 ... -20 16 -32 ... ... process_time_diff (chain, draw) float64 16kB 0.004583 ... 0.004648 reached_max_treedepth (chain, draw) bool 2kB False False ... False False smallest_eigval (chain, draw) float64 16kB nan nan nan ... nan nan step_size (chain, draw) float64 16kB 0.09049 ... 0.07296 step_size_bar (chain, draw) float64 16kB 0.07765 ... 0.09081 tree_depth (chain, draw) int64 16kB 6 5 6 5 5 6 ... 6 5 6 5 6 6 Attributes: created_at: 2026-02-03T20:55:06.902207+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 sampling_time: 8.357609987258911 tuning_steps: 1000 -

<xarray.Dataset> Size: 3kB Dimensions: (date: 179) Coordinates: * date (date) datetime64[ns] 1kB 2018-04-02 2018-04-09 ... 2021-08-30 Data variables: y (date) float64 1kB 0.5317 0.6001 0.6019 ... 0.3418 0.2982 0.2264 Attributes: created_at: 2026-02-03T20:55:06.904767+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 -

<xarray.Dataset> Size: 9kB Dimensions: (date: 179, channel: 2, control: 2) Coordinates: * date (date) datetime64[ns] 1kB 2018-04-02 ... 2021-08-30 * channel (channel) <U2 16B 'x1' 'x2' * control (control) <U7 56B 'event_1' 'event_2' Data variables: channel_data (date, channel) float64 3kB 0.2948 0.0 0.9383 ... 0.1269 0.0 channel_scale (channel) float64 16B 0.9968 0.9927 control_data (date, control) float64 3kB 0.0 0.0 0.0 0.0 ... 0.0 0.0 0.0 dayofyear (date) int32 716B 92 99 106 113 120 ... 214 221 228 235 242 target_data (date) float64 1kB 7.784 8.785 8.812 ... 5.004 4.366 3.315 target_scale float64 8B 14.64 Attributes: created_at: 2026-02-03T20:55:06.906425+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 -

<xarray.Dataset> Size: 9kB Dimensions: (date_week: 179) Coordinates: * date_week (date_week) datetime64[ns] 1kB 2018-04-02 ... 2021-08-30 Data variables: x1 (date_week) float64 1kB 0.2948 0.9383 0.1397 ... 0.9364 0.1269 x2 (date_week) float64 1kB 0.0 0.0 0.0 0.0 0.0 ... 0.0 0.0 0.0 0.0 event_1 (date_week) float64 1kB 0.0 0.0 0.0 0.0 0.0 ... 0.0 0.0 0.0 0.0 event_2 (date_week) float64 1kB 0.0 0.0 0.0 0.0 0.0 ... 0.0 0.0 0.0 0.0 y (date_week) float64 1kB 7.784 8.785 8.812 ... 5.004 4.366 3.315

As we can see the model found divergencies!🤯

The occurrence of divergences in our Bayesian MMM highlights the strengths and robustness of the Bayesian framework in hypothesis testing and model validation. Bayesian models are structural and adhere to certain assumptions about the data-generating process. When these assumptions are violated or the model structure does not fit the data well, divergences and sampling problems can arise.

This characteristic makes the Bayesian approach a powerful tool for:

Hypothesis Testing: By defining clear structural relationships and assumptions, Bayesian models can help test and validate hypotheses about the underlying processes in the data.

Model Validation: Divergences and sampling issues serve as indicators that the model may not be correctly specified, prompting further investigation and refinement.

Understanding Complex Systems: Bayesian methods allow for the incorporation of prior knowledge and the testing of various structural assumptions, making them well-suited for understanding complex, real-world systems.

In this particular case, we can perfectly suspect why the model had divergences. The internal structure from our world model (MMM) is neglecting time when this one is an important factor (we know this because we have carried out the due process of data generation).

Despite that, let’s take a look at the data that we were able to recover through this basic model.

If we decompose the posterior predictive distribution into the different components, everything becomes clear:

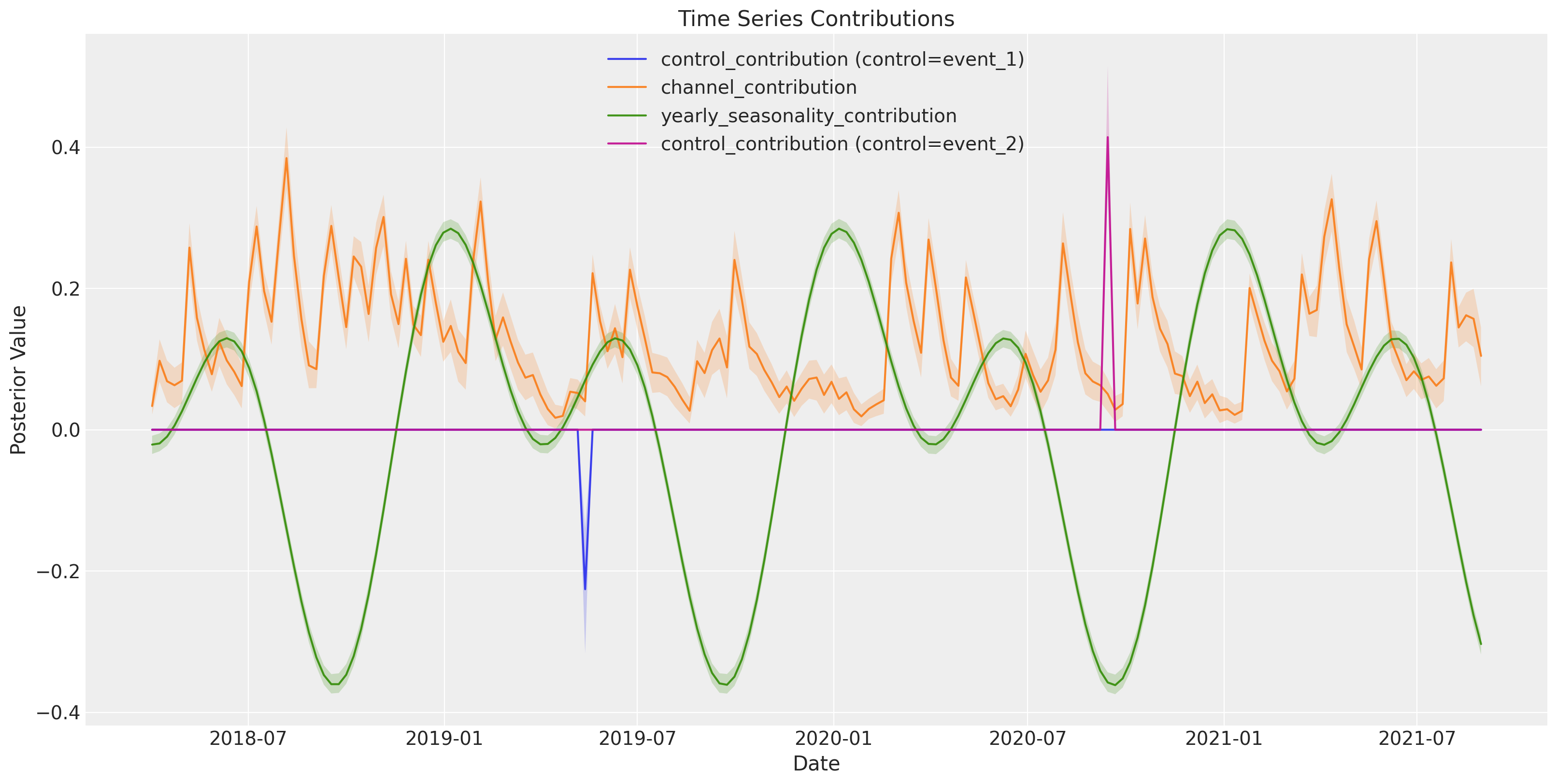

basic_mmm.plot.contributions_over_time(

var=[

"control_contribution",

"channel_contribution",

"yearly_seasonality_contribution",

],

combine_dims=True,

figsize=(16, 8),

)

(<Figure size 1600x800 with 1 Axes>,

array([[<Axes: title={'center': 'Time Series Contributions'}, xlabel='Date', ylabel='Posterior Value'>]],

dtype=object))

Some contributions end up having more units than the target value, forcing the model to compensate. Resulting in an incorrect decomposition of our marketing activities.

For example, our time series ends up with a long tail of probable values for marketing contributions, this tail being up to 3X greater than the maximum value of our target.

def plot_posterior(

posterior, figsize=(15, 8), path_color="blue", hist_color="blue", **kwargs

):

"""Plot the posterior distribution of a stochastic process.

Parameters

----------

posterior : xarray.DataArray

The posterior distribution with shape (draw, chain, date).

figsize : tuple

Size of the figure.

path_color : str

Color of the paths in the time series plot.

hist_color : str

Color of the histogram.

**kwargs

Additional keyword arguments to pass to the plotting functions.

"""

# Calculate the expected value (mean) across all draws and chains for each date

expected_value = posterior.mean(dim=("draw", "chain"))

# Create a figure and a grid of subplots

fig = plt.figure(figsize=figsize)

gs = fig.add_gridspec(1, 2, width_ratios=[3, 1])

# Time series plot

ax1 = fig.add_subplot(gs[0])

for chain in range(posterior.shape[1]):

for draw in range(

0, posterior.shape[0], 10

): # Plot every 10th draw for performance

ax1.plot(

posterior.date,

posterior[draw, chain],

color=path_color,

alpha=0.05,

linewidth=0.4,

)

# Plot expected value with a distinct color

ax1.plot(

posterior.date,

expected_value,

color="black",

linestyle="--",

linewidth=2,

label="Expected Value",

)

ax1.set_title("Posterior Predictive")

ax1.set_xlabel("Date")

ax1.set_ylabel("Value")

ax1.grid(True)

ax1.legend()

# KDE plot instead of histogram

ax2 = fig.add_subplot(gs[1])

final_values = posterior[:, :, -1].values.flatten()

sns.kdeplot(

y=final_values, ax=ax2, color=hist_color, fill=True, alpha=0.4, **kwargs

)

# Plot expected value line in KDE plot

ax2.axhline(

y=expected_value[-1].values.mean(), color="black", linestyle="--", linewidth=2

)

ax2.set_title("Distribution at T")

ax2.set_xlabel("Density")

ax2.set_yticklabels([]) # Hide y tick labels to avoid duplication

ax2.grid(True)

plt.tight_layout()

return fig

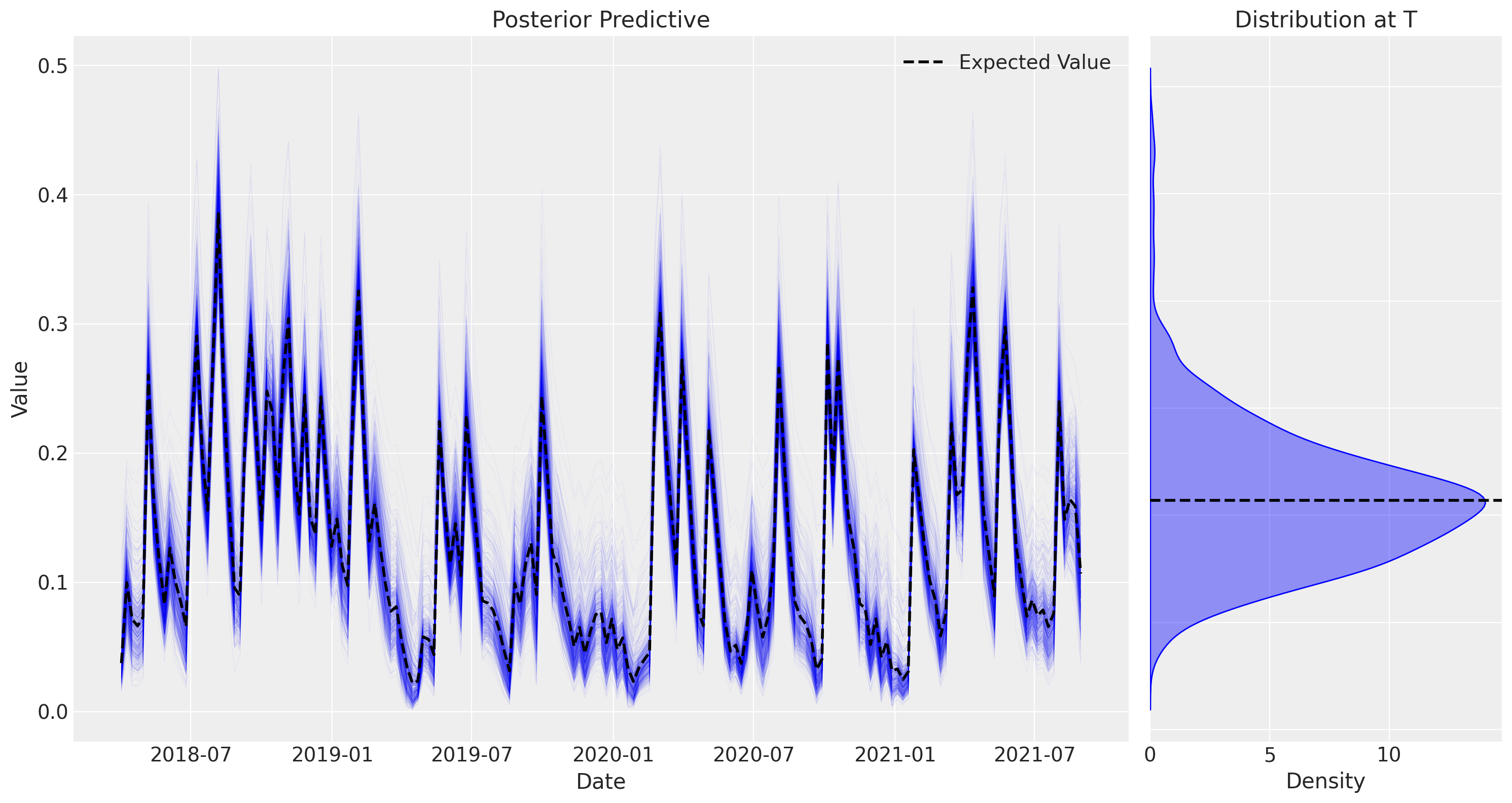

plot_posterior(

posterior=basic_mmm.fit_result["channel_contribution"].sum(dim="channel")

);

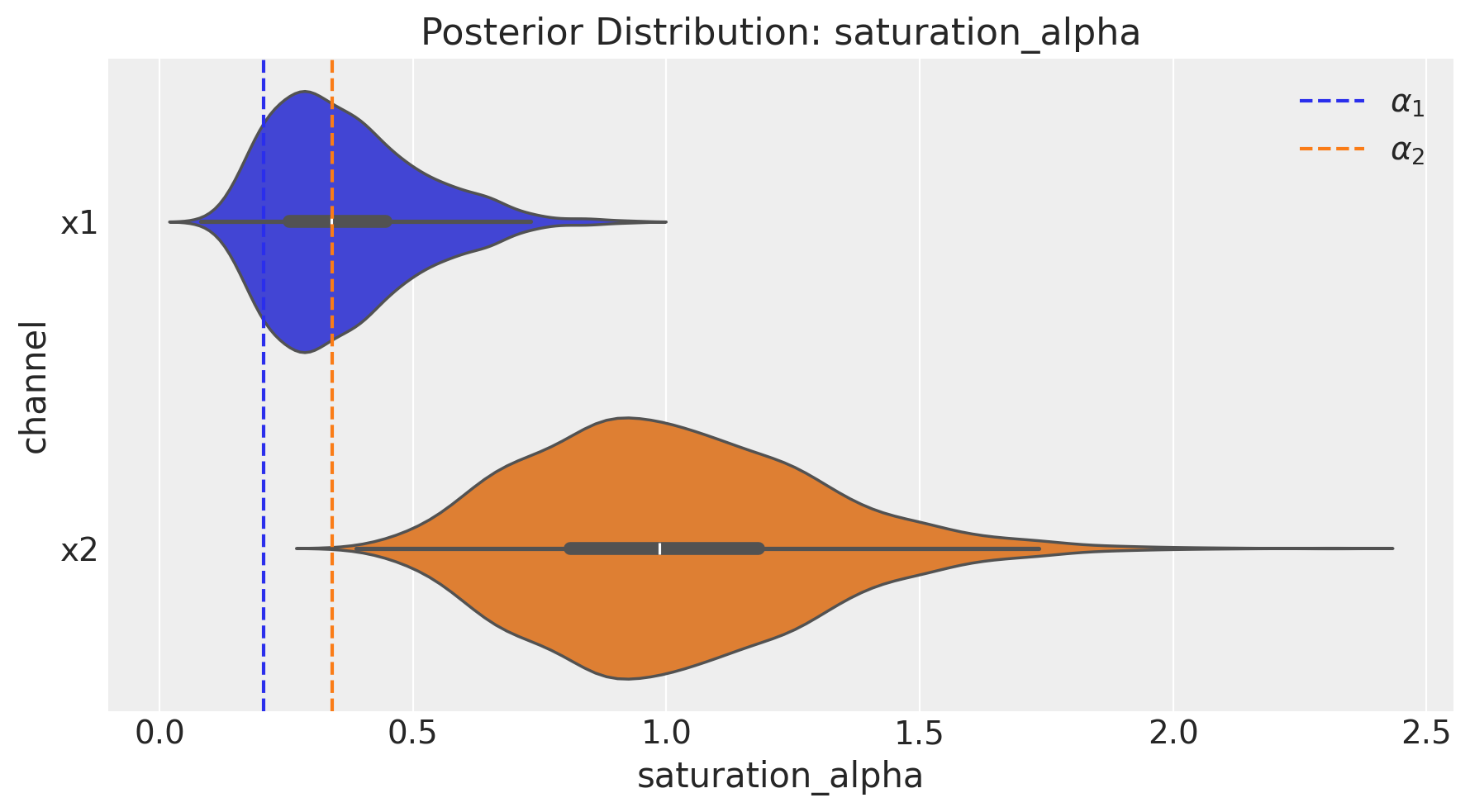

But why the contributions are over estimated? The contributions are poorly estimated because the parameters of our transformations are also poorly estimated. For example, the parameters that control the maximum effectiveness (At the saturation function) of each channel are much higher than the real ones for both channels.

fig = basic_mmm.plot.channel_parameter(param_name="saturation_alpha", figsize=(9, 5))

ax = fig.axes[0]

ax.axvline(

x=(real_alpha[0] / df.y.max()), color="C0", linestyle="--", label=r"$\alpha_1$"

)

ax.axvline(

x=(real_alpha[1] / df.y.max()), color="C1", linestyle="--", label=r"$\alpha_2$"

)

ax.legend(loc="upper right");

What would change if we now consider time as a factor in our model?

Now we can do this by adding the following parameter to the initialization of our time_varying_media model and changing it to True.

from pymc_marketing.hsgp_kwargs import HSGPKwargs

hsgp_kwargs = HSGPKwargs(

ls_mu=11.0, # InverseGamma lengthscale prior mean

ls_sigma=5.0, # InverseGamma lengthscale prior sigma

)

mmm = MMM(

date_column="date_week",

target_column="y",

channel_columns=["x1", "x2"],

control_columns=["event_1", "event_2"],

yearly_seasonality=yearly_seasonality,

adstock=GeometricAdstock(l_max=adstock_max_lag).set_dims_for_all_priors("channel"),

saturation=MichaelisMentenSaturation().set_dims_for_all_priors("channel"),

time_varying_media=True, # 1. Enable the feature

model_config={"media_tvp_config": hsgp_kwargs},

)

Note

By doing this, now our model config will have a new key media_tvp_config with the parameters that control the priors of our HSGP.

mmm.model_config["media_tvp_config"]

HSGPKwargs(m=200, L=None, eta_lam=1, ls_mu=11.0, ls_sigma=5.0, cov_func=None)

mmm.fit(

X=X,

y=y,

target_accept=0.92,

draws=500,

random_seed=rng,

)

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [intercept_contribution, adstock_alpha, saturation_alpha, saturation_lam, media_temporal_latent_multiplier_raw_eta, media_temporal_latent_multiplier_raw_ls, media_temporal_latent_multiplier_raw_hsgp_coefs_offset, gamma_control, gamma_fourier, y_sigma]

Sampling 4 chains for 1_000 tune and 500 draw iterations (4_000 + 2_000 draws total) took 54 seconds.

There were 8 divergences after tuning. Increase `target_accept` or reparameterize.

The rhat statistic is larger than 1.01 for some parameters. This indicates problems during sampling. See https://arxiv.org/abs/1903.08008 for details

-

<xarray.Dataset> Size: 44MB Dimensions: (chain: 4, draw: 500, channel: 2, control: 2, fourier_mode: 4, media_temporal_latent_multiplier_raw_m: 200, date: 179) Coordinates: * chain (chain) int64 32B ... * draw (draw) int64 4kB ... * channel (channel) <U2 16B ... * control (control) <U7 56B ... * fourier_mode (fourier_mode) <U5 80B ... * media_temporal_latent_multiplier_raw_m (media_temporal_latent_multiplier_raw_m) int64 2kB ... * date (date) datetime64[ns] 1kB ... Data variables: (12/20) adstock_alpha (chain, draw, channel) float64 32kB ... gamma_control (chain, draw, control) float64 32kB ... gamma_fourier (chain, draw, fourier_mode) float64 64kB ... intercept_contribution (chain, draw) float64 16kB ... media_temporal_latent_multiplier_raw_eta (chain, draw) float64 16kB ... media_temporal_latent_multiplier_raw_hsgp_coefs_offset (chain, draw, media_temporal_latent_multiplier_raw_m) float64 3MB ... ... ... media_temporal_latent_multiplier (chain, draw, date) float64 3MB ... media_temporal_latent_multiplier_f_mean (chain, draw) float64 16kB ... media_temporal_latent_multiplier_raw (chain, draw, date) float64 3MB ... media_temporal_latent_multiplier_raw_hsgp_coefs (chain, draw, media_temporal_latent_multiplier_raw_m) float64 3MB ... total_media_contribution_original_scale (chain, draw) float64 16kB ... yearly_seasonality_contribution (chain, draw, date) float64 3MB ... Attributes: created_at: 2026-02-03T20:56:17.140137+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 sampling_time: 54.1484808921814 tuning_steps: 1000 pymc_marketing_version: 0.17.1 -

<xarray.Dataset> Size: 264kB Dimensions: (chain: 4, draw: 500) Coordinates: * chain (chain) int64 32B 0 1 2 3 * draw (draw) int64 4kB 0 1 2 3 4 5 ... 495 496 497 498 499 Data variables: (12/18) acceptance_rate (chain, draw) float64 16kB 0.9151 0.9345 ... 0.9902 divergences (chain, draw) int64 16kB 0 0 0 0 0 0 ... 2 2 2 2 2 2 diverging (chain, draw) bool 2kB False False ... False False energy (chain, draw) float64 16kB -41.24 -41.99 ... -58.52 energy_error (chain, draw) float64 16kB 0.08577 ... 0.002545 index_in_trajectory (chain, draw) int64 16kB 84 -20 47 ... 47 -91 -102 ... ... process_time_diff (chain, draw) float64 16kB 0.02821 ... 0.02846 reached_max_treedepth (chain, draw) bool 2kB False False ... False False smallest_eigval (chain, draw) float64 16kB nan nan nan ... nan nan step_size (chain, draw) float64 16kB 0.02866 ... 0.03422 step_size_bar (chain, draw) float64 16kB 0.03508 ... 0.03673 tree_depth (chain, draw) int64 16kB 7 7 7 7 7 7 ... 7 7 7 7 7 7 Attributes: created_at: 2026-02-03T20:56:17.151157+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 sampling_time: 54.1484808921814 tuning_steps: 1000 -

<xarray.Dataset> Size: 3kB Dimensions: (date: 179) Coordinates: * date (date) datetime64[ns] 1kB 2018-04-02 2018-04-09 ... 2021-08-30 Data variables: y (date) float64 1kB 0.5317 0.6001 0.6019 ... 0.3418 0.2982 0.2264 Attributes: created_at: 2026-02-03T20:56:17.154293+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 -

<xarray.Dataset> Size: 10kB Dimensions: (date: 179, channel: 2, control: 2) Coordinates: * date (date) datetime64[ns] 1kB 2018-04-02 ... 2021-08-30 * channel (channel) <U2 16B 'x1' 'x2' * control (control) <U7 56B 'event_1' 'event_2' Data variables: channel_data (date, channel) float64 3kB 0.2948 0.0 0.9383 ... 0.1269 0.0 channel_scale (channel) float64 16B 0.9968 0.9927 control_data (date, control) float64 3kB 0.0 0.0 0.0 0.0 ... 0.0 0.0 0.0 dayofyear (date) int32 716B 92 99 106 113 120 ... 214 221 228 235 242 target_data (date) float64 1kB 7.784 8.785 8.812 ... 5.004 4.366 3.315 target_scale float64 8B 14.64 time_index (date) int32 716B 0 1 2 3 4 5 6 ... 173 174 175 176 177 178 Attributes: created_at: 2026-02-03T20:56:17.156463+00:00 arviz_version: 0.23.0 inference_library: pymc inference_library_version: 5.27.0 -

<xarray.Dataset> Size: 9kB Dimensions: (date_week: 179) Coordinates: * date_week (date_week) datetime64[ns] 1kB 2018-04-02 ... 2021-08-30 Data variables: x1 (date_week) float64 1kB 0.2948 0.9383 0.1397 ... 0.9364 0.1269 x2 (date_week) float64 1kB 0.0 0.0 0.0 0.0 0.0 ... 0.0 0.0 0.0 0.0 event_1 (date_week) float64 1kB 0.0 0.0 0.0 0.0 0.0 ... 0.0 0.0 0.0 0.0 event_2 (date_week) float64 1kB 0.0 0.0 0.0 0.0 0.0 ... 0.0 0.0 0.0 0.0 y (date_week) float64 1kB 7.784 8.785 8.812 ... 5.004 4.366 3.315

We got less divergences, this is a good sign! 🚀

Let’s check our samples!

az.summary(

data=mmm.fit_result,

var_names=[

"intercept_contribution",

"y_sigma",

"gamma_control",

"gamma_fourier",

],

)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| intercept_contribution | 0.413 | 0.007 | 0.399 | 0.427 | 0.0 | 0.0 | 1988.0 | 1471.0 | 1.0 |

| y_sigma | 0.017 | 0.001 | 0.015 | 0.018 | 0.0 | 0.0 | 2915.0 | 1413.0 | 1.0 |

| gamma_control[event_1] | -0.251 | 0.018 | -0.283 | -0.216 | 0.0 | 0.0 | 2957.0 | 1418.0 | 1.0 |

| gamma_control[event_2] | 0.431 | 0.018 | 0.396 | 0.461 | 0.0 | 0.0 | 3626.0 | 1549.0 | 1.0 |

| gamma_fourier[sin_1] | 0.169 | 0.003 | 0.163 | 0.175 | 0.0 | 0.0 | 1692.0 | 1071.0 | 1.0 |

| gamma_fourier[sin_2] | -0.032 | 0.002 | -0.036 | -0.028 | 0.0 | 0.0 | 3111.0 | 1390.0 | 1.0 |

| gamma_fourier[cos_1] | 0.100 | 0.003 | 0.095 | 0.106 | 0.0 | 0.0 | 2112.0 | 1164.0 | 1.0 |

| gamma_fourier[cos_2] | 0.172 | 0.002 | 0.168 | 0.176 | 0.0 | 0.0 | 2836.0 | 1752.0 | 1.0 |

_ = az.plot_trace(

data=mmm.fit_result,

var_names=[

"intercept_contribution",

"y_sigma",

"gamma_control",

"gamma_fourier",

],

compact=True,

backend_kwargs={"figsize": (12, 10), "layout": "constrained"},

)

plt.gcf().suptitle("Model Trace", fontsize=16);

az.summary(

data=mmm.fit_result,

var_names=["adstock_alpha", "saturation_lam", "saturation_alpha"],

)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

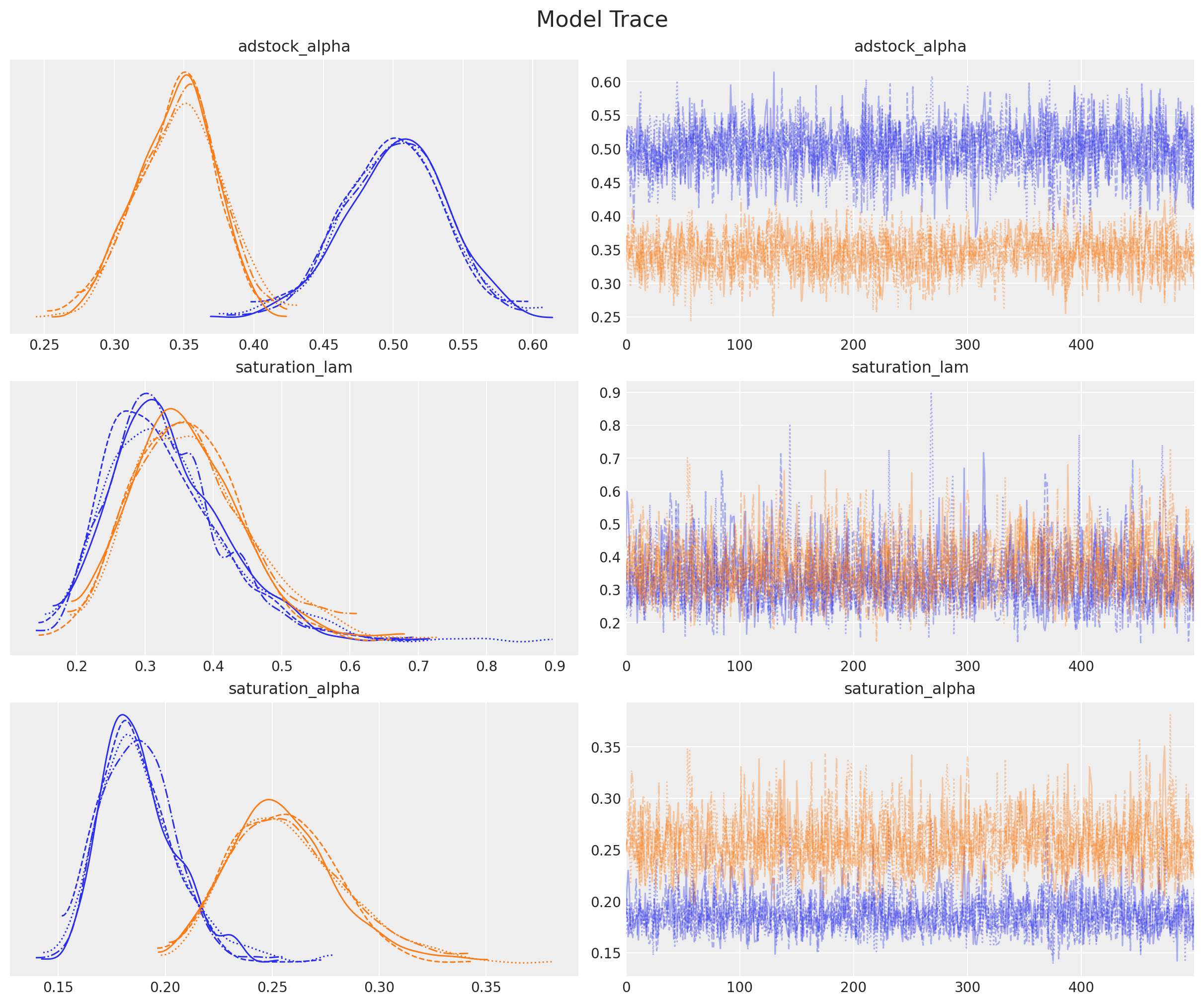

| adstock_alpha[x1] | 0.500 | 0.038 | 0.423 | 0.569 | 0.001 | 0.001 | 1976.0 | 1653.0 | 1.0 |

| adstock_alpha[x2] | 0.345 | 0.029 | 0.287 | 0.395 | 0.001 | 0.001 | 1426.0 | 1444.0 | 1.0 |

| saturation_lam[x1] | 0.333 | 0.091 | 0.182 | 0.502 | 0.002 | 0.003 | 1582.0 | 1193.0 | 1.0 |

| saturation_lam[x2] | 0.366 | 0.085 | 0.202 | 0.519 | 0.002 | 0.002 | 1357.0 | 1282.0 | 1.0 |

| saturation_alpha[x1] | 0.188 | 0.018 | 0.158 | 0.222 | 0.000 | 0.001 | 1539.0 | 1158.0 | 1.0 |

| saturation_alpha[x2] | 0.256 | 0.026 | 0.211 | 0.307 | 0.001 | 0.001 | 1316.0 | 1180.0 | 1.0 |

_ = az.plot_trace(

data=mmm.fit_result,

var_names=["adstock_alpha", "saturation_lam", "saturation_alpha"],

compact=True,

backend_kwargs={"figsize": (12, 10), "layout": "constrained"},

)

plt.gcf().suptitle("Model Trace", fontsize=16);

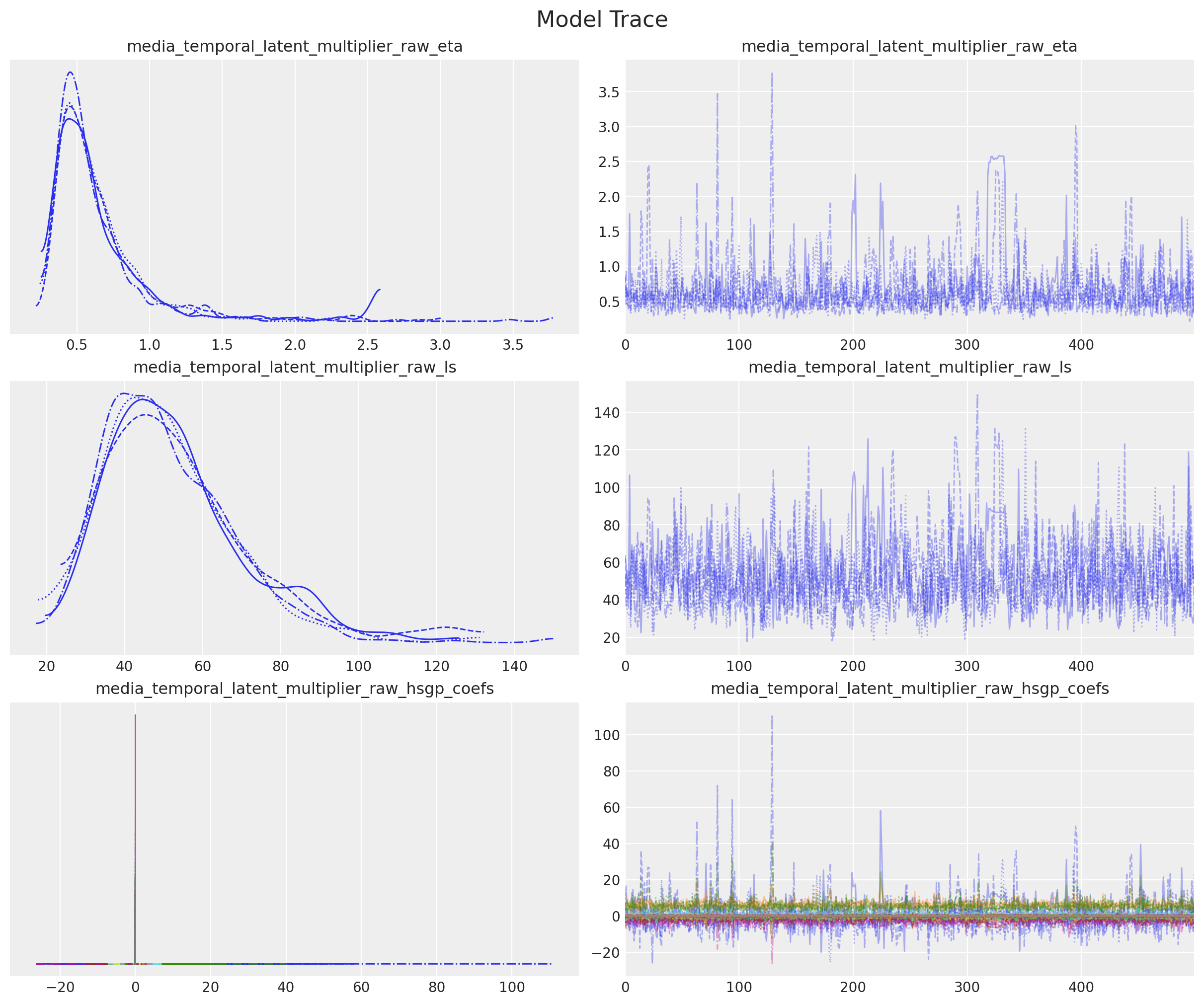

az.summary(

data=mmm.fit_result,

var_names=[

"media_temporal_latent_multiplier_raw_eta",

"media_temporal_latent_multiplier_raw_ls",

"media_temporal_latent_multiplier_raw_hsgp_coefs",

],

)

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| media_temporal_latent_multiplier_raw_eta | 0.643 | 0.364 | 0.242 | 1.201 | 0.018 | 0.041 | 944.0 | 542.0 | 1.01 |

| media_temporal_latent_multiplier_raw_ls | 52.133 | 17.904 | 25.169 | 86.925 | 0.666 | 0.668 | 792.0 | 482.0 | 1.01 |

| media_temporal_latent_multiplier_raw_hsgp_coefs[0] | 0.140 | 8.410 | -14.409 | 12.980 | 0.210 | 0.545 | 1996.0 | 1173.0 | 1.00 |

| media_temporal_latent_multiplier_raw_hsgp_coefs[1] | 6.197 | 1.938 | 2.813 | 9.697 | 0.048 | 0.069 | 1749.0 | 1378.0 | 1.00 |

| media_temporal_latent_multiplier_raw_hsgp_coefs[2] | 5.361 | 2.909 | 0.956 | 10.262 | 0.070 | 0.160 | 1836.0 | 1317.0 | 1.00 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| media_temporal_latent_multiplier_raw_hsgp_coefs[195] | -0.000 | 0.000 | -0.000 | 0.000 | 0.000 | 0.000 | 2914.0 | 1565.0 | 1.00 |

| media_temporal_latent_multiplier_raw_hsgp_coefs[196] | 0.000 | 0.000 | -0.000 | 0.000 | 0.000 | 0.000 | 3106.0 | 1518.0 | 1.01 |

| media_temporal_latent_multiplier_raw_hsgp_coefs[197] | -0.000 | 0.000 | -0.000 | 0.000 | 0.000 | 0.000 | 4220.0 | 1427.0 | 1.00 |

| media_temporal_latent_multiplier_raw_hsgp_coefs[198] | -0.000 | 0.000 | -0.000 | 0.000 | 0.000 | 0.000 | 3287.0 | 1454.0 | 1.00 |

| media_temporal_latent_multiplier_raw_hsgp_coefs[199] | 0.000 | 0.000 | -0.000 | 0.000 | 0.000 | 0.000 | 3258.0 | 1591.0 | 1.01 |

202 rows × 9 columns

_ = az.plot_trace(

data=mmm.fit_result,

var_names=[

"media_temporal_latent_multiplier_raw_eta",

"media_temporal_latent_multiplier_raw_ls",

"media_temporal_latent_multiplier_raw_hsgp_coefs",

],

compact=True,

backend_kwargs={"figsize": (12, 10), "layout": "constrained"},

)

plt.gcf().suptitle("Model Trace", fontsize=16);

Everything seems fine for now, there is nothing that raises red flags when analyzing our trace. But what about the decomposition?

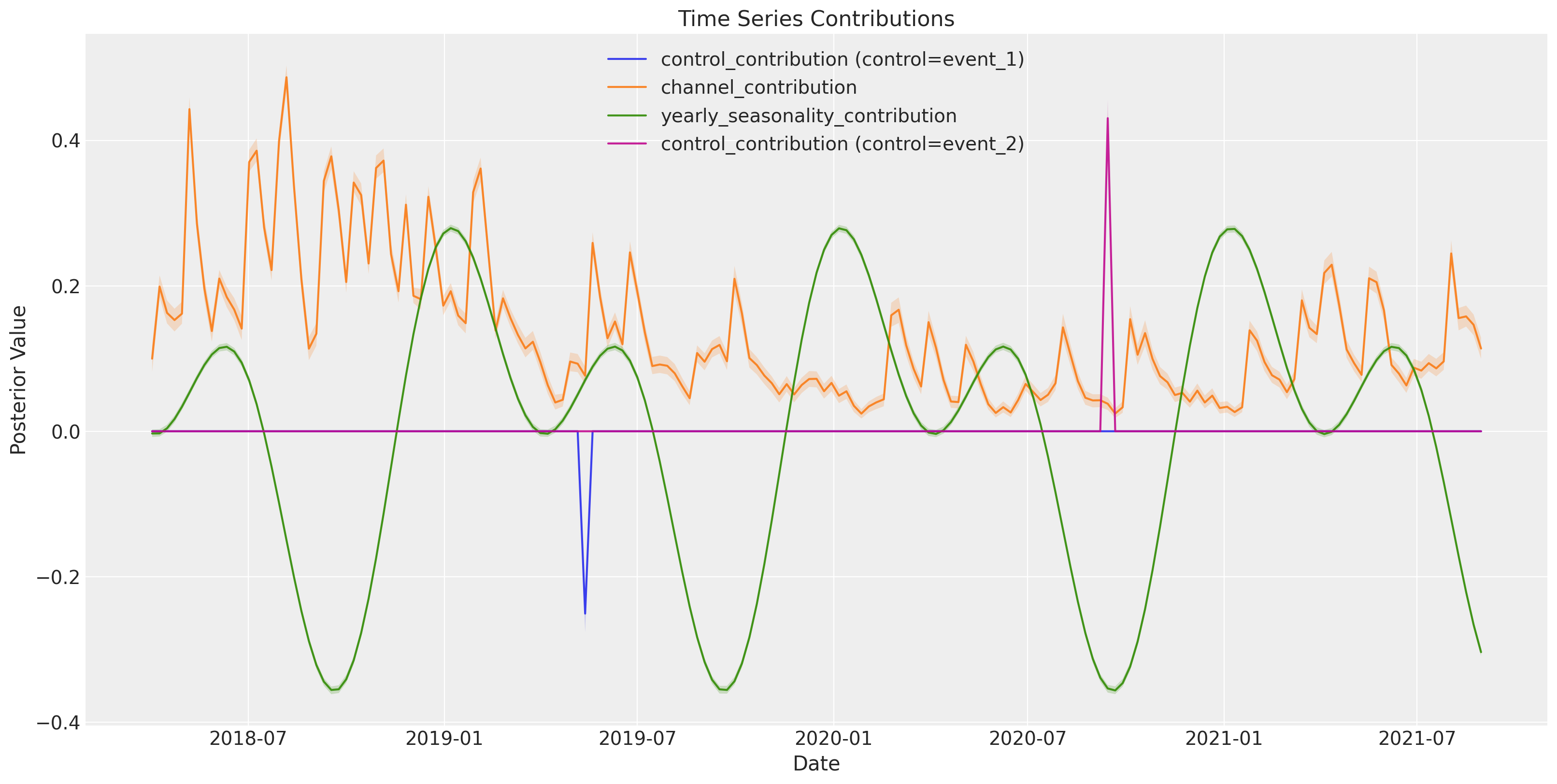

mmm.plot.contributions_over_time(

var=[

"control_contribution",

"channel_contribution",

"yearly_seasonality_contribution",

],

combine_dims=True,

figsize=(16, 8),

);

The decomposition looks much better now 🔥 It seems that we are estimating each parameter better, and there are no obvious trade-offs between components!

Let’s see how well the original parameters have managed to be recovered?

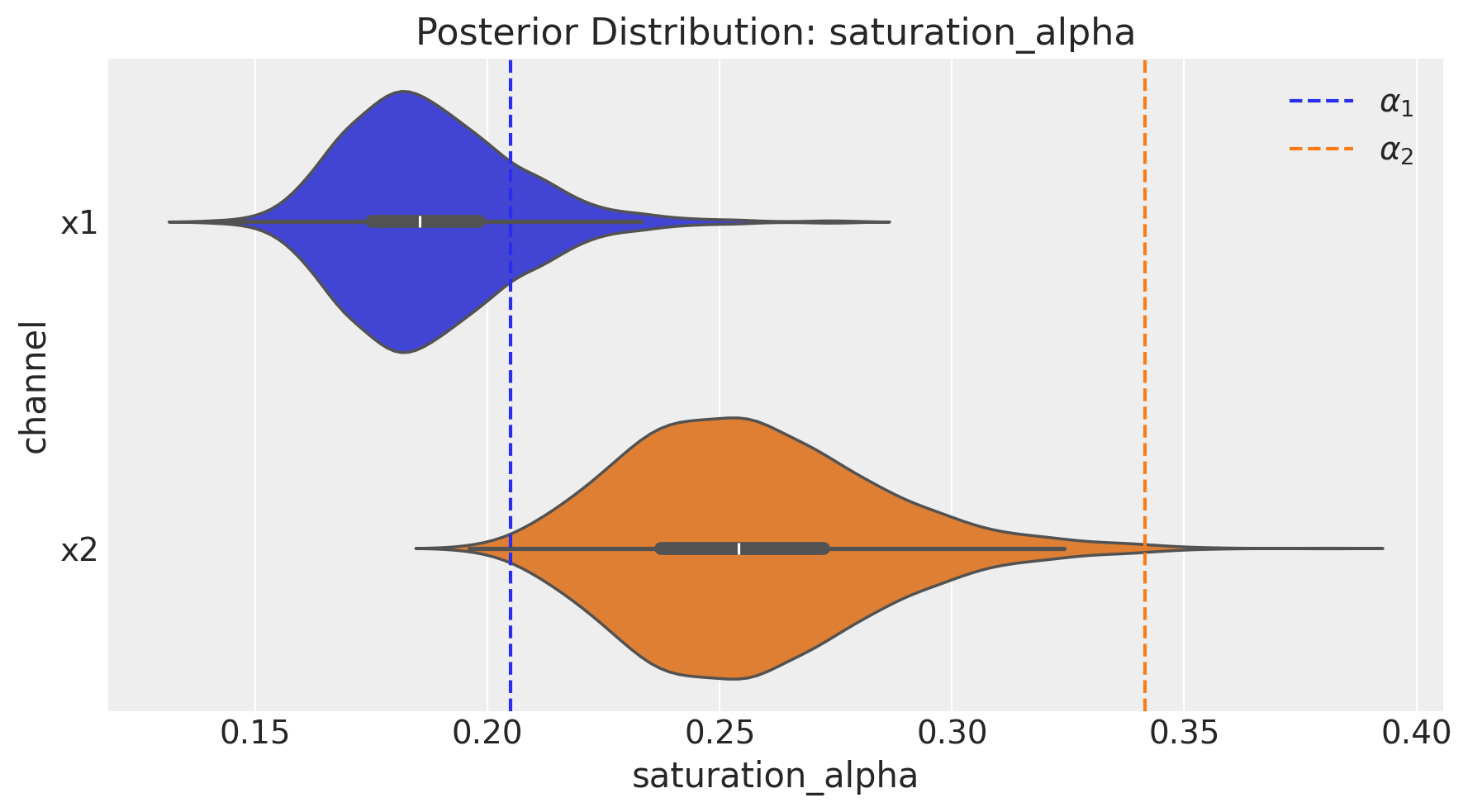

fig = mmm.plot.channel_parameter(param_name="saturation_alpha", figsize=(9, 5))

ax = fig.axes[0]

ax.axvline(

x=(real_alpha[0] / df.y.max()), color="C0", linestyle="--", label=r"$\alpha_1$"

)

ax.axvline(

x=(real_alpha[1] / df.y.max()), color="C1", linestyle="--", label=r"$\alpha_2$"

)

ax.legend(loc="upper right");

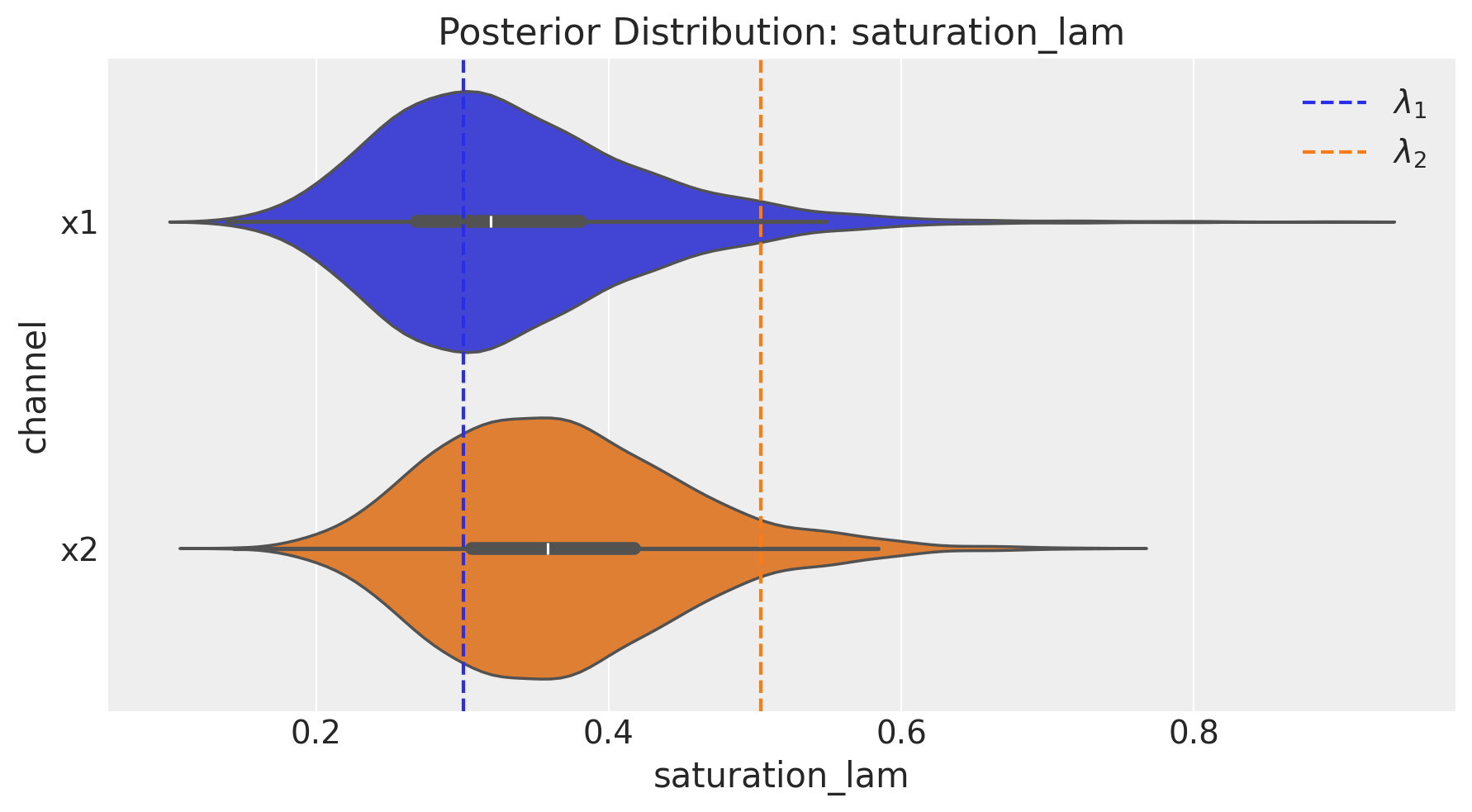

fig = mmm.plot.channel_parameter(param_name="saturation_lam", figsize=(9, 5))

ax = fig.axes[0]

ax.axvline(

x=(real_lam[0] / df.x1.max()), color="C0", linestyle="--", label=r"$\lambda_1$"

)

ax.axvline(

x=(real_lam[1] / df.x2.max()), color="C1", linestyle="--", label=r"$\lambda_2$"

)

ax.legend(loc="upper right");

The parameters of the saturation function seem to be recovered practically in their entirety for both channels! This is great 🎉

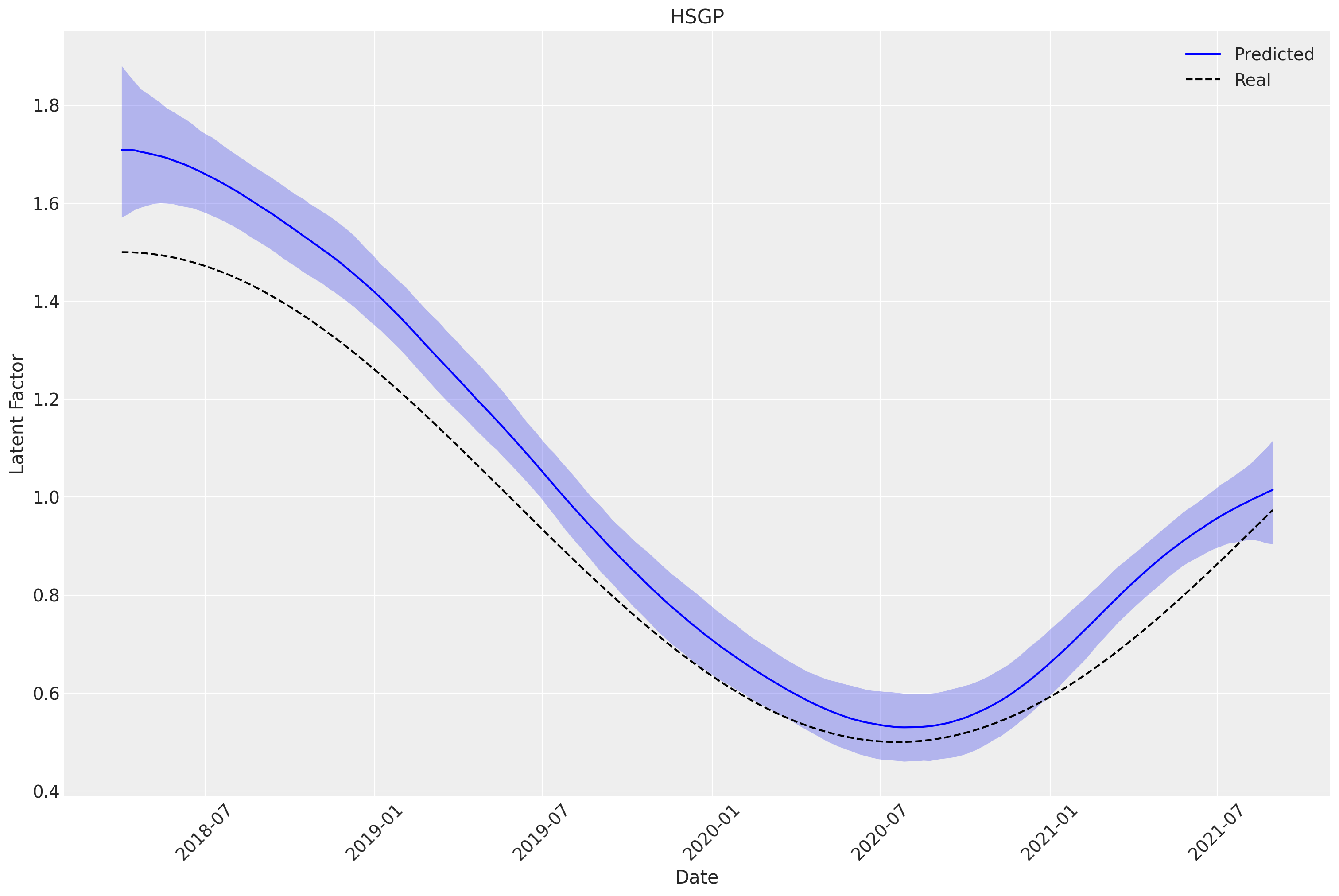

Let’s see how much we manage to recover from the true variation. We can analyze the variable media_temporal_latent_multiplier and compare it against the original variable used in the original process.

media_latent_factor = mmm.fit_result["media_temporal_latent_multiplier"].quantile(

[0.025, 0.50, 0.975], dim=["chain", "draw"]

)

fig, ax = plt.subplots(nrows=1, ncols=1, figsize=(15, 10))

sns.lineplot(

x=mmm.fit_result.coords["date"],

y=media_latent_factor.sel(quantile=0.5),

label="Predicted",

color="blue",

)

sns.lineplot(

x=mmm.fit_result.coords["date"],

y=df["hidden_latent_media_fluctuation"],

label="Real",

color="Black",

linestyle="--",

)

ax.fill_between(

mmm.fit_result.coords["date"],

media_latent_factor.sel(quantile=0.025),

media_latent_factor.sel(quantile=0.975),

alpha=0.3,

)

ax.set_title("HSGP")

ax.set_xlabel("Date")

ax.set_ylabel("Latent Factor")

ax.tick_params(axis="x", rotation=45)

ax.legend()

plt.show()

Incredible 🚀 we recovered the latent process almost perfectly. Although it seems a little overestimated, it is quite close to the real thing!

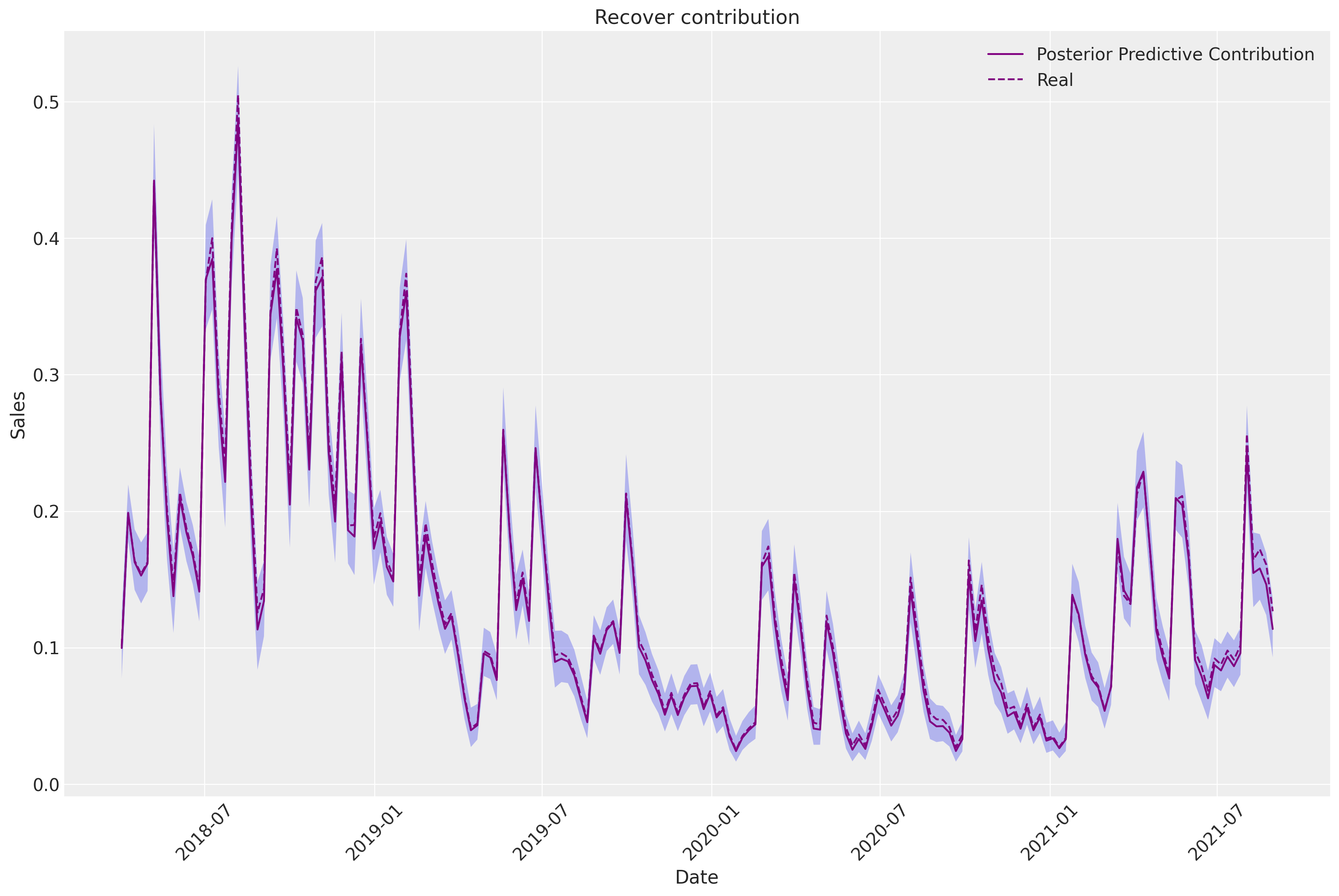

recover_channel_contribution = mmm.fit_result["channel_contribution"].quantile(

[0.025, 0.50, 0.975], dim=["chain", "draw"]

)

fig, ax = plt.subplots(nrows=1, ncols=1, figsize=(15, 10))

sns.lineplot(

x=mmm.fit_result.coords["date"],

y=recover_channel_contribution.sel(quantile=0.5).sum(axis=-1),

label="Posterior Predictive Contribution",

color="purple",

)

sns.lineplot(

x=mmm.fit_result.coords["date"],

y=df["channel_contribution"] / df["y"].max(),

label="Real",

color="purple",

linestyle="--",

)

ax.fill_between(

mmm.fit_result.coords["date"],

recover_channel_contribution.sel(quantile=0.025).sum(axis=-1),

recover_channel_contribution.sel(quantile=0.975).sum(axis=-1),

alpha=0.3,

)

ax.set_title("Recover contribution")

ax.set_xlabel("Date")

ax.set_ylabel("Sales")

ax.tick_params(axis="x", rotation=45)

ax.legend()

plt.show()

This is reflected when comparing the recovered contribution against the original. We can see that they are exactly the same!

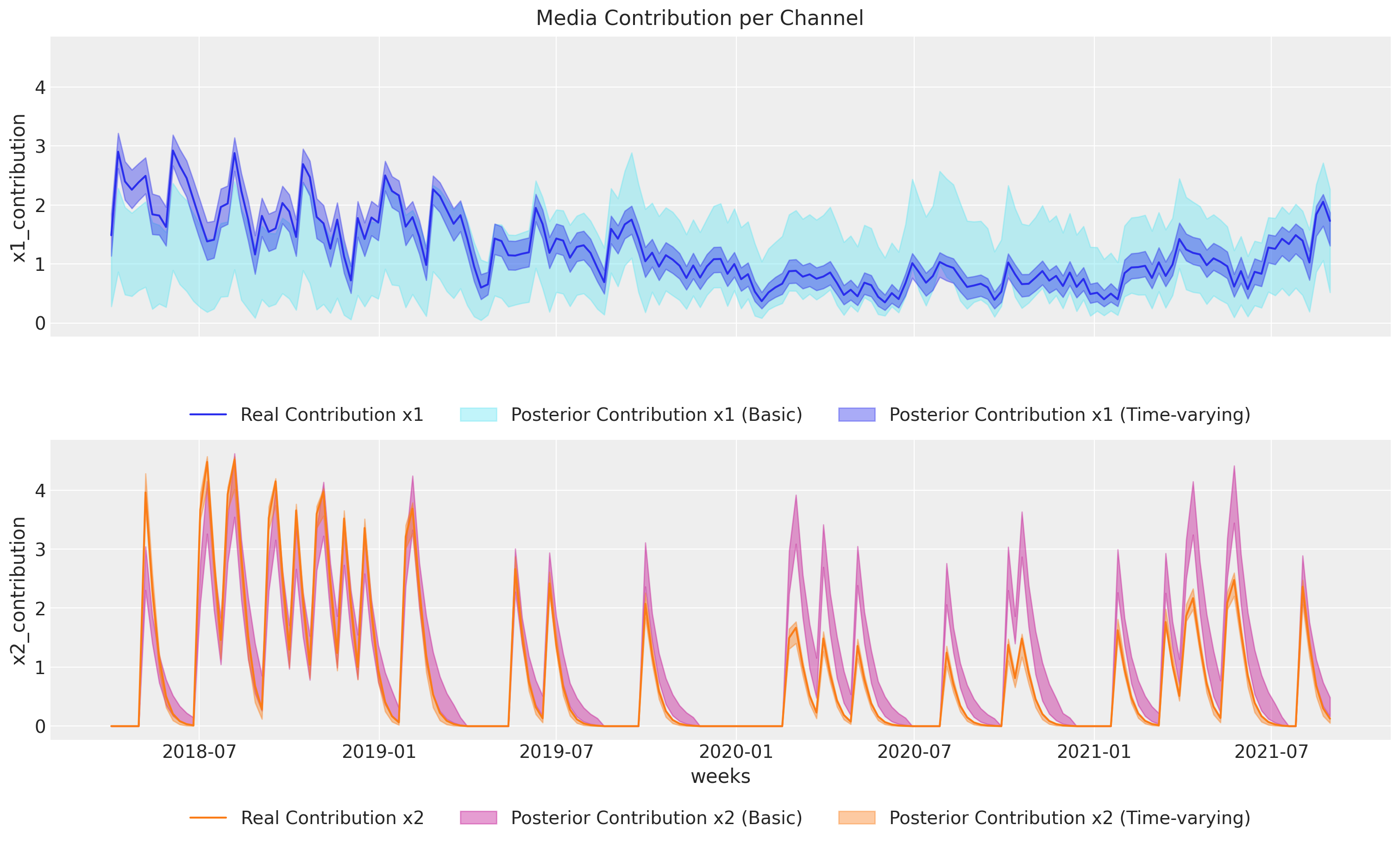

We can compare now the contributions split by channel between our two models.

basic_recover_channel_contribution = basic_mmm.fit_result[

"channel_contribution"

].quantile([0.025, 0.50, 0.975], dim=["chain", "draw"])

fig, ax = plt.subplots(

nrows=2, ncols=1, figsize=(15, 9), sharex=True, sharey=True, layout="constrained"

)

sns.lineplot(

x="date_week",

y="x1_contribution",

data=df,

color="C0",

ax=ax[0],

label="Real Contribution x1",

)

ax[0].fill_between(

basic_mmm.fit_result.coords["date"],

basic_recover_channel_contribution.sel(quantile=0.025).sel(channel="x1")

* df.y.max(),

basic_recover_channel_contribution.sel(quantile=0.975).sel(channel="x1")

* df.y.max(),

alpha=0.4,

color="C5",

label="Posterior Contribution x1 (Basic)",

)

ax[0].fill_between(

mmm.fit_result.coords["date"],

recover_channel_contribution.sel(quantile=0.025).sel(channel="x1") * df.y.max(),

recover_channel_contribution.sel(quantile=0.975).sel(channel="x1") * df.y.max(),

alpha=0.4,

color="C0",

label="Posterior Contribution x1 (Time-varying)",

)

ax[0].legend(bbox_to_anchor=(0.5, -0.18), loc="upper center", ncols=3)

sns.lineplot(

x="date_week",

y="x2_contribution",

data=df,

color="C1",

ax=ax[1],

label="Real Contribution x2",

)

ax[1].fill_between(

basic_mmm.fit_result.coords["date"],

basic_recover_channel_contribution.sel(quantile=0.025).sel(channel="x2")

* df.y.max(),

basic_recover_channel_contribution.sel(quantile=0.975).sel(channel="x2")

* df.y.max(),

alpha=0.4,

color="C3",

label="Posterior Contribution x2 (Basic)",

)

ax[1].fill_between(

mmm.fit_result.coords["date"],

recover_channel_contribution.sel(quantile=0.025).sel(channel="x2") * df.y.max(),

recover_channel_contribution.sel(quantile=0.975).sel(channel="x2") * df.y.max(),

alpha=0.4,

color="C1",

label="Posterior Contribution x2 (Time-varying)",

)

ax[1].set(xlabel="weeks")

fig.suptitle("Media Contribution per Channel", fontsize=16)

ax[1].legend(bbox_to_anchor=(0.5, -0.18), loc="upper center", ncols=3);

Contributions per channel were also recovered correctly, unlike our first model! Actually, we see how the base model tries (and fails!) to capture the true variation. The reason is clear: lack of flexibility.

Insights#

The Bayesian approach not only facilitates hypothesis testing and model validation but also provides a structured way to incorporate prior knowledge and test various assumptions about the data-generating process. The occurrence of divergences, as observed in our initial model fitting, underscores the importance of model specification and alignment with the underlying data structure. These divergences serve as a diagnostic tool, guiding further refinement and improvement of the model.

In summary, using PyMC-Marketing to build time-aware MMM models enables marketers to gain deeper insights and achieve a more accurate understanding of the impact of their efforts. This methodology enhances the ability to make data-driven decisions, optimize marketing strategies, and ultimately drive better business outcomes.

Conclusion#

Throughout this notebook, we have explored the implementation of a Bayesian Marketing Mix Model (MMM) using PyMC, comparing the performance and insights gained from models with and without a time component. The key takeaway from our analysis is the significant advantage of incorporating time-varying factors into MMM.

Uncovering Real Causal Relationships#

By integrating a time component, we can uncover the true causal relationships between our target variable (such as sales) and our marketing efforts. The traditional approach, which neglects temporal dynamics, often fails to capture the complex and fluctuating nature of real-world marketing performance. In contrast, the time-dependent model provides a more accurate and nuanced understanding of how marketing activities influence outcomes over time.

Advantages of PyMC-Marketing#

PyMC-Marketing, offers powerful tools to implement these advanced methodologies. The new features and functionalities, including the handling differents adstock effects, saturation effects, and Hilbert Space Gaussian processes (HSGP) for modeling time-varying components, allow for more precise and reliable modeling of marketing data.

We encourage practitioners to leverage these advanced techniques and the capabilities of PyMC-Marketing to improve their marketing analytics and gain a competitive edge in their strategic planning.

Bonus#

This notebook simulated a very simple variation, it is possible that the true time-dependent latent processes hidden in your data are more complex therefore, you will need to use priors to guide your model to find the real data.

One way to achieve this is through modifying the model configuration.

custom_config = {

"intercept": Prior("HalfNormal", sigma=0.5),

"saturation_alpha": Prior(

"Gamma", mu=np.array([0.3, 0.4]), sigma=np.array([0.2, 0.2]), dims="channel"

),

"saturation_lam": Prior("Beta", alpha=4, beta=4, dims="channel"),

}

media_tvp_config = {

"media_tvp_config": {

"m": 50,

"L": 30,

"eta_lam": 3,

"ls_mu": 5,

"ls_sigma": 5,

"cov_func": None,

}

}

custom_config = {**mmm.model_config, **custom_config, **media_tvp_config}

custom_config

{'intercept': Prior("HalfNormal", sigma=0.5),

'likelihood': Prior("Normal", sigma=Prior("HalfNormal", sigma=2), dims="date"),

'gamma_control': Prior("Normal", mu=0, sigma=2, dims="control"),

'gamma_fourier': Prior("Laplace", mu=0, b=1, dims="fourier_mode"),

'media_tvp_config': {'m': 50,

'L': 30,

'eta_lam': 3,

'ls_mu': 5,

'ls_sigma': 5,

'cov_func': None},

'adstock_alpha': Prior("Beta", alpha=1, beta=3, dims="channel"),

'saturation_alpha': Prior("Gamma", mu=[0.3 0.4], sigma=[0.2 0.2], dims="channel"),

'saturation_lam': Prior("Beta", alpha=4, beta=4, dims="channel")}

mmm_calibrated = MMM(

date_column="date_week",

target_column="y",

channel_columns=["x1", "x2"],

control_columns=["event_1", "event_2"],

yearly_seasonality=yearly_seasonality,

adstock=GeometricAdstock(l_max=adstock_max_lag),

saturation=MichaelisMentenSaturation(),

time_varying_media=True,

model_config=custom_config,

)

%load_ext watermark

%watermark -n -u -v -iv -w -p pymc,pymc_marketing,pytensor,numpyro

Last updated: Tue, 03 Feb 2026

Python implementation: CPython

Python version : 3.13.11

IPython version : 9.9.0

pymc : 5.27.0

pymc_marketing: 0.17.1

pytensor : 2.36.3

numpyro : 0.19.0

arviz : 0.23.0

matplotlib : 3.10.8

numpy : 2.3.5

pandas : 2.3.3

pymc_extras : 0.7.0

pymc_marketing: 0.17.1

seaborn : 0.13.2

Watermark: 2.6.0