Shifted Beta Geometric model with individual customer data#

In this notebook we replicate the main results and figures from

Fader, P. S., & Hardie, B. G. (2007). How to project customer retention. Journal of Interactive Marketing, 21(1), 76-90. https://journals.sagepub.com/doi/pdf/10.1002/dir.20074

The authors describe the Shifted Beta Geometric (sBG) model for customer behavior in a discrete contractual setting. It assumes that:

At the end of each period, a customer has a probability

thetaof renewing the contract and1-thetaof cancellingThe probability

thetadoes not change over time for a given customerThe probability

thetavaries across customers according to a Beta prior distribution with hyperparametersalphaandbeta.

import arviz as az

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import xarray as xr

from pymc_marketing import clv

# Plotting configuration

az.style.use("arviz-darkgrid")

plt.rcParams["figure.figsize"] = [12, 7]

plt.rcParams["figure.dpi"] = 100

plt.rcParams["figure.facecolor"] = "white"

%load_ext autoreload

%autoreload 2

%config InlineBackend.figure_format = "retina"

seed = sum(map(ord, "Individual sBG Model"))

rng = np.random.default_rng(seed)

Recreating the dataset#

The dataset contains the percentage of customers still enrolled in the service after each time period. There are two distinct groups of users: regular and high-end, believed to have different attrition rates. Each group had 1000 customers at the start.

As in the original paper, we will fit the data from the first 7 time periods only, and use the following periods for validation.

df = pd.DataFrame(

{

"regular": [

100.0,

63.1,

46.8,

38.2,

32.6,

28.9,

26.2,

24.1,

22.3,

20.7,

19.4,

18.3,

17.3,

],

"highend": [

100.0,

86.9,

74.3,

65.3,

59.3,

55.1,

51.7,

49.1,

46.8,

44.5,

42.7,

40.9,

39.4,

],

}

)

df

| regular | highend | |

|---|---|---|

| 0 | 100.0 | 100.0 |

| 1 | 63.1 | 86.9 |

| 2 | 46.8 | 74.3 |

| 3 | 38.2 | 65.3 |

| 4 | 32.6 | 59.3 |

| 5 | 28.9 | 55.1 |

| 6 | 26.2 | 51.7 |

| 7 | 24.1 | 49.1 |

| 8 | 22.3 | 46.8 |

| 9 | 20.7 | 44.5 |

| 10 | 19.4 | 42.7 |

| 11 | 18.3 | 40.9 |

| 12 | 17.3 | 39.4 |

The implemented pymc-marketing model fits each individual theta,

in contrast to the paper approach where the inidividual parameters are marginalized out.

For our analysis we wil have to create a synthetic dataset with individual data, following the aggregate group trends.

def individual_data_from_percentage_alive(percentage_alive, initial_customers):

n_alive = np.asarray(percentage_alive / 100 * initial_customers, dtype=int)

died_at = np.zeros((initial_customers,), dtype=int)

counter = 0

for t, diff in enumerate((n_alive[:-1] - n_alive[1:]), start=1):

died_at[counter : counter + diff] = t

counter += diff

censoring_t = t + 1

died_at[counter:] = censoring_t

return died_at

T = 8 # In the paper only the first 7 years are included in the model

truncated_df = df[:T]

initial_customers = 1000 # Seems to be what F&H use, according to Appendix B

churn_highend = individual_data_from_percentage_alive(

truncated_df["highend"], initial_customers

)

churn_regular = individual_data_from_percentage_alive(

truncated_df["regular"], initial_customers

)

churn_regular[::10]

array([1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1,

1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 2, 2, 2, 2, 2, 2, 2,

2, 2, 2, 2, 2, 2, 2, 2, 2, 2, 3, 3, 3, 3, 3, 3, 3, 3, 4, 4, 4, 4,

4, 4, 5, 5, 5, 5, 6, 6, 7, 7, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8,

8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8, 8])

Customers which haven’t churned have t_churn == T == 8.

The model will handle these differently, as their lifetimes are censored.

Fitting the sBG models for high end and regular users#

dataset_highend = pd.DataFrame(

{

"customer_id": np.arange(initial_customers) + 1,

"t_churn": churn_highend,

"T": T,

"cohorts": "highend",

}

)

highend_users = clv.ShiftedBetaGeoModelIndividual()

highend_users.build_model(data=dataset_highend)

highend_users

Shifted-Beta-Geometric Model (Individual Customers)

alpha ~ HalfFlat()

beta ~ HalfFlat()

theta ~ Beta(alpha, beta)

churn_censored ~ Censored(Geometric(theta), -inf, <constant>)

dataset_regular = pd.DataFrame(

{

"customer_id": np.arange(initial_customers) + 1001,

"t_churn": churn_regular,

"T": T,

"cohorts": "regular",

}

)

regular_users = clv.ShiftedBetaGeoModelIndividual()

regular_users.build_model(data=dataset_regular)

regular_users

Shifted-Beta-Geometric Model (Individual Customers)

alpha ~ HalfFlat()

beta ~ HalfFlat()

theta ~ Beta(alpha, beta)

churn_censored ~ Censored(Geometric(theta), -inf, <constant>)

highend_users.fit(random_seed=rng, nuts_sampler="nutpie")

regular_users.fit(random_seed=rng, nuts_sampler="nutpie");

Sampler Progress

Total Chains: 4

Active Chains: 0

Finished Chains: 4

Sampling for now

Estimated Time to Completion: now

| Progress | Draws | Divergences | Step Size | Gradients/Draw |

|---|---|---|---|---|

| 2000 | 0 | 0.23 | 15 | |

| 2000 | 0 | 0.24 | 15 | |

| 2000 | 0 | 0.23 | 15 | |

| 2000 | 0 | 0.23 | 15 |

Sampler Progress

Total Chains: 4

Active Chains: 0

Finished Chains: 4

Sampling for now

Estimated Time to Completion: now

| Progress | Draws | Divergences | Step Size | Gradients/Draw |

|---|---|---|---|---|

| 2000 | 0 | 0.26 | 15 | |

| 2000 | 0 | 0.25 | 15 | |

| 2000 | 0 | 0.26 | 15 | |

| 2000 | 0 | 0.26 | 15 |

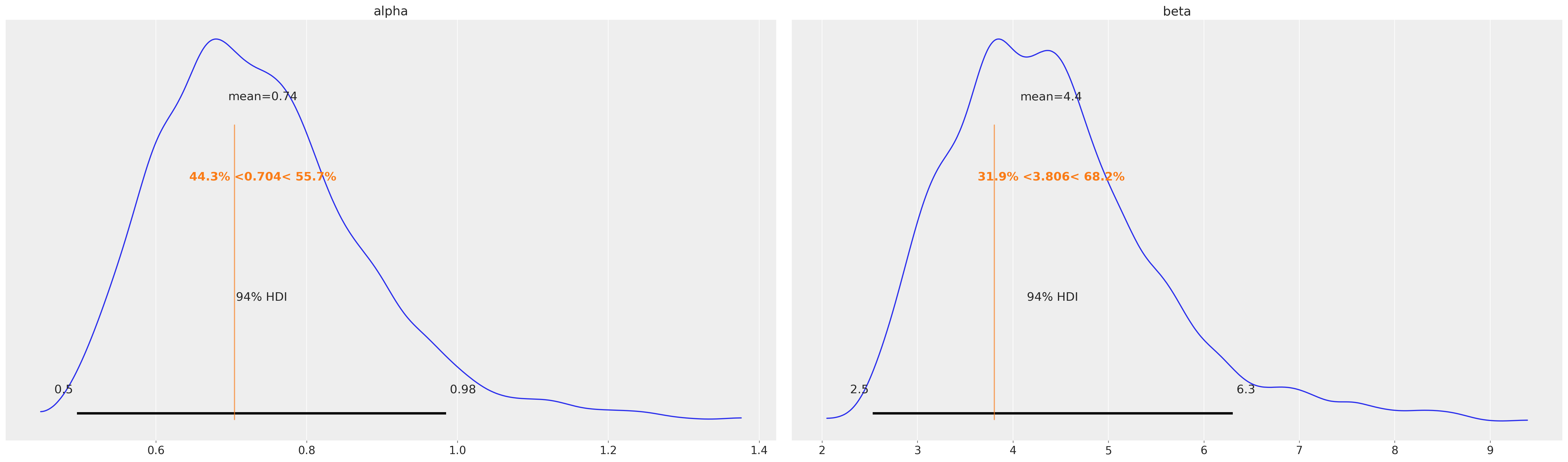

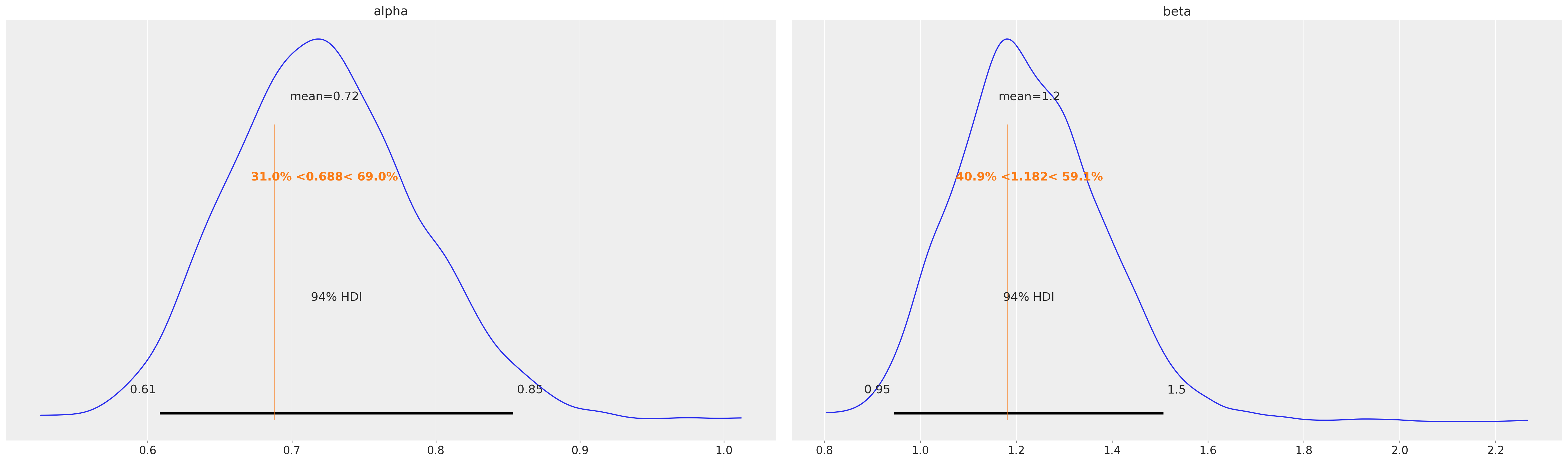

Contrasting posterior inferences with the repo MLE estimates#

The sBG model has 2 population parameters of interest: alpha and beta.

These parameters define the population distribution of the individual customer’s churn rates theta.

The larger the values of alpha and beta the more homogenous the churn rates are across different customers.

The ratio of alpha to beta tells us the expected churn rates. If alpha/beta == 0.1, we expect the average customer to have a 0.1 probability of churning between each time period.

# MLE estimates from the paper

ref_val = {

"highend": [0.704, 3.806],

"regular": [0.688, 1.182],

}

highend_users.fit_summary(var_names=["alpha", "beta"])

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| alpha | 0.742 | 0.139 | 0.495 | 0.985 | 0.017 | 0.011 | 71.0 | 152.0 | 1.06 |

| beta | 4.400 | 1.087 | 2.530 | 6.304 | 0.128 | 0.087 | 73.0 | 141.0 | 1.06 |

az.plot_posterior(

highend_users.fit_result, var_names=["alpha", "beta"], ref_val=ref_val["highend"]

);

regular_users.fit_summary(var_names=["alpha", "beta"])

| mean | sd | hdi_3% | hdi_97% | mcse_mean | mcse_sd | ess_bulk | ess_tail | r_hat | |

|---|---|---|---|---|---|---|---|---|---|

| alpha | 0.723 | 0.067 | 0.608 | 0.854 | 0.004 | 0.002 | 225.0 | 589.0 | 1.02 |

| beta | 1.228 | 0.157 | 0.945 | 1.507 | 0.011 | 0.007 | 214.0 | 577.0 | 1.02 |

az.plot_posterior(

regular_users.fit_result, var_names=["alpha", "beta"], ref_val=ref_val["regular"]

);

The model fitting agrees with the Maximum Likelihood estimates described in the original paper. In addition, MCMC sampling, gives us useful information about the uncertainty of the fits.

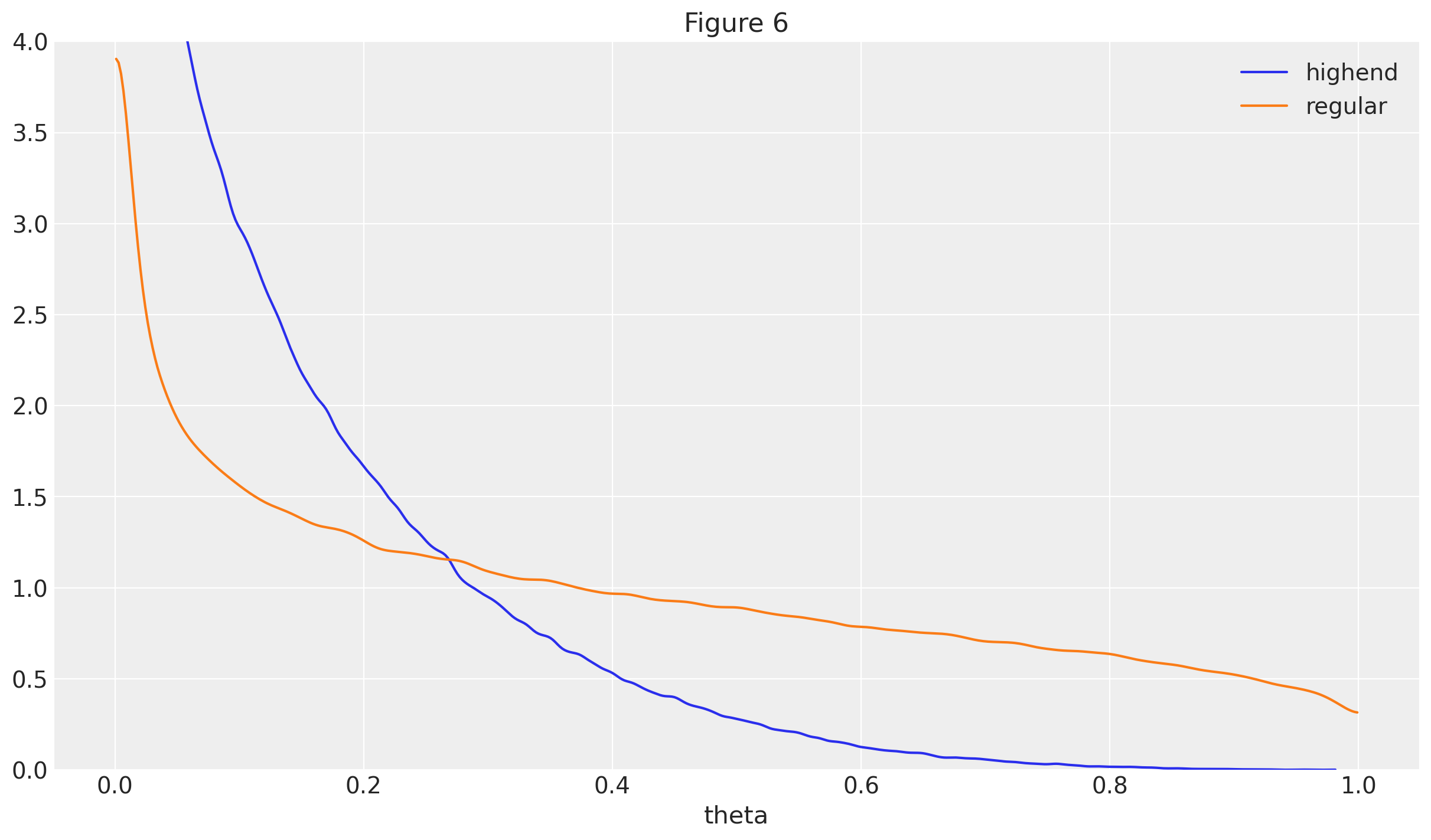

Recreating main results and figures from the paper#

Figure 6 from the paper shows the group distribution of theta churn rates.

The inferred distributions are relatively wide in both groups, which follows directly from the fact that both alpha and beta were inferred to be < 10.

It is still clear that the distribution of theta for the highend users has much more mass near lower values,

suggesting highend users have lower attrition rates on average, when compared with regular users.

new_highend_theta = highend_users.distribution_new_customer_theta(

n=100, random_seed=rng

)

new_regular_theta = regular_users.distribution_new_customer_theta(

n=100, random_seed=rng

);

Sampling: [theta]

Sampling: [theta]

ax = az.plot_dist(new_highend_theta, label="highend")

ax = az.plot_dist(new_regular_theta, label="regular", ax=ax, color="C1")

ax.set_xlabel("theta")

plt.ylim([0, 4])

ax.set_title("Figure 6");

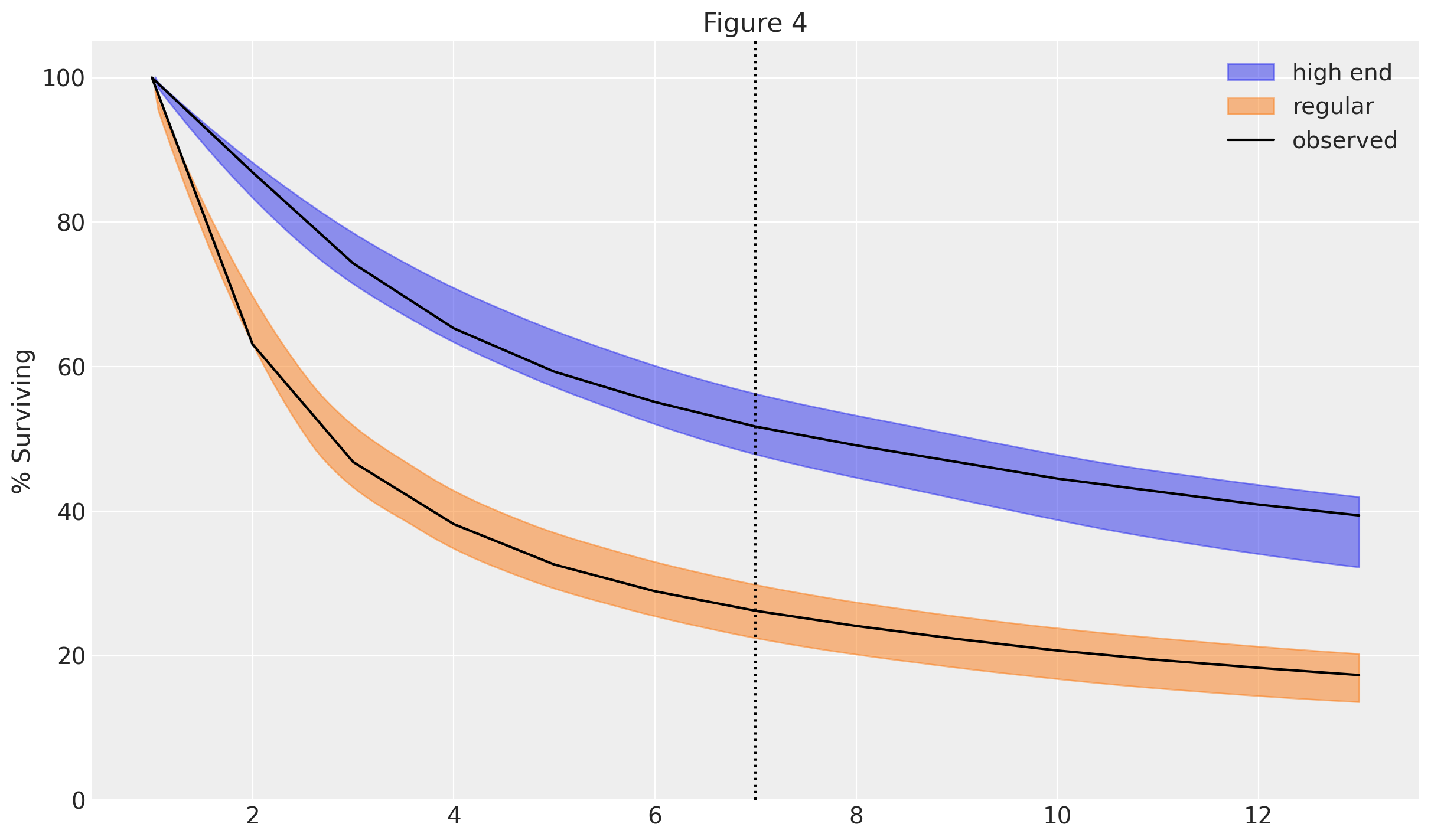

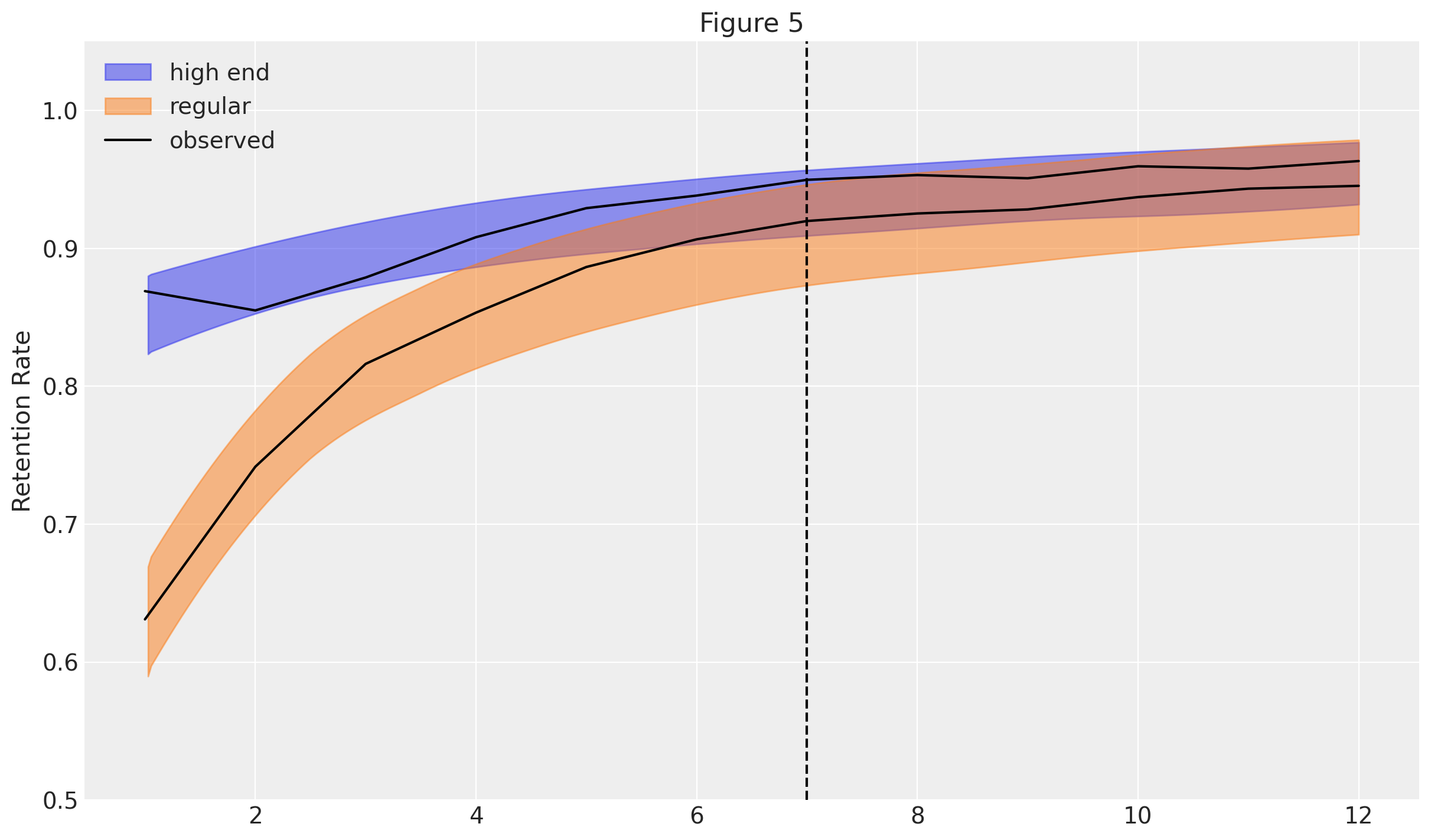

Figures 4 and 5 show the predicted average churn and retention trends for the two groups. We can see that predictions nicely match the observed data (black line), even when extrapolating into the time periods that were held-out when fitting the model.

The plots also highlight an interesting implication from the model: the retention rates are expected to increase over time, as the more precarious customers gradually drop out. This is a direct consequence of modelling individual churn rates as being fixed over time.

churn_highend = highend_users.distribution_customer_churn_time(

customer_id=np.arange(initial_customers),

random_seed=rng,

)

churn_regular = regular_users.distribution_customer_churn_time(

customer_id=np.arange(initial_customers),

random_seed=rng,

)

Sampling: [churn, theta]

Sampling: [churn, theta]

weeks = xr.DataArray(np.arange(1, 14), dims=["weeks"])

survival_perc_highend = 100 - 100 * (churn_highend < weeks)

survival_perc_regular = 100 - 100 * (churn_regular < weeks)

az.plot_hdi(

weeks,

survival_perc_highend.mean("customer_id"),

hdi_prob=0.95,

color="C0",

fill_kwargs={"label": "high end"},

)

az.plot_hdi(

weeks,

survival_perc_regular.mean("customer_id"),

hdi_prob=0.95,

color="C1",

fill_kwargs={"label": "regular"},

)

plt.plot(weeks, df["highend"], color="k", label="observed")

plt.plot(weeks, df["regular"], color="k")

plt.axvline(7, ls=":", color="k")

plt.ylim([0, 105])

plt.ylabel("% Surviving")

plt.legend()

plt.title("Figure 4");

retention_rate_highend = survival_perc_highend.isel(

weeks=slice(1, None, None)

) / survival_perc_highend.isel(weeks=slice(None, -1, None))

retention_rate_regular = survival_perc_regular.isel(

weeks=slice(1, None, None)

) / survival_perc_regular.isel(weeks=slice(None, -1, None))

retention_rate_highend_obs = df["highend"][1:].values / df["highend"][:-1].values

retention_rate_regular_obs = df["regular"][1:].values / df["regular"][:-1].values

weeks_ = weeks[:-1]

az.plot_hdi(

weeks_,

retention_rate_highend.mean("customer_id"),

hdi_prob=0.95,

color="C0",

fill_kwargs={"label": "high end"},

)

az.plot_hdi(

weeks_,

retention_rate_regular.mean("customer_id"),

hdi_prob=0.95,

color="C1",

fill_kwargs={"label": "regular"},

)

plt.plot(weeks_, retention_rate_highend_obs, color="k", label="observed")

plt.plot(weeks_, retention_rate_regular_obs, color="k")

plt.axvline(7, ls="--", color="k")

plt.ylim([0.5, 1.05])

plt.ylabel("Retention Rate")

plt.legend()

plt.title("Figure 5");

%load_ext watermark

%watermark -n -u -v -iv -w -p pymc,pytensor

The watermark extension is already loaded. To reload it, use:

%reload_ext watermark

Last updated: Thu Oct 16 2025

Python implementation: CPython

Python version : 3.12.11

IPython version : 9.4.0

pymc : 5.25.1

pytensor: 2.31.7

arviz : 0.22.0

numpy : 2.2.6

pandas : 2.3.1

xarray : 2025.7.1

pymc_marketing: 0.15.1

pytensor : 2.31.7

matplotlib : 3.10.3

Watermark: 2.5.0